A trust is a legal entity that holds assets, such as a home, for the benefit of others. It is created by a settler or grantor, who transfers ownership to a trustee. When a house is placed in a trust, it becomes part of the trust’s estate and is managed according to the terms outlined in the trust documents, which are verified through trust certifications. The trustee is then responsible for overseeing the property and acting in the best interests of the beneficiary.

To sell a house held in a trust, the trustee must confirm authority, follow legal procedures, and protect the beneficiaries’ interests. If a beneficiary inherits a home but prefers to sell it instead of maintaining it, the trustee oversees the entire process. This includes obtaining beneficiary consent, working with an escrow company, managing the title transfer, and completing the Trustee’s Deed Upon Sale. When handled correctly, this helps avoid probate and ensures a faster, legally valid sale.

Understanding how to sell a house in a trust helps prevent tax complications, ensure legal compliance, and protect beneficiary rights. The next sections explain key legal factors, tax rules, and the practical steps trustees can follow to complete the sale efficiently.

What Are the Things to Consider When Selling a House in Trust?

When selling a house in a trust, consider trustee authority, beneficiary consent, legal compliance, and tax obligations. The trustee must verify the right to sell through the trust documents and trust certifications, follow state laws, and ensure the title transfer is handled correctly. Addressing these elements early helps prevent legal disputes, delays, and financial complications for both the trustee and the beneficiaries.

Tax Implications of Selling a House in a Trust

The sale of a house in a trust follows different tax rules than a standard home sale, mainly involving capital gains, property tax reassessment, and inheritance or estate taxes. The impact depends on the trust type and how the property was used. If it were a primary residence, certain exclusions may lower the taxable profit. Working with a tax advisor helps the trustee manage these obligations correctly and keep the sale compliant.

- Capital Gains Tax

When a trust sells a property for more than its original purchase price, the profit is usually subject to capital gains tax. In a revocable trust, the grantor reports the gain, while an irrevocable trust may owe it directly. If the home was a primary residence, the IRS capital gains exclusion allows up to $250,000 for individuals or $500,000 for married couples to be tax-free. Understanding these limits helps the trustee reduce tax exposure and distribute proceeds correctly.

- Property Tax Reassessment

Selling a home held in a trust often triggers a property tax reassessment for the new owner once the title transfer is recorded. The county assessor revalues the property at its current market price, which can raise annual taxes if the home has appreciated. In California, Proposition 13 limits yearly increases to 2%, but a sale resets the assessed value to market level. The trustee should disclose this potential change and check if any parent-child exclusion or similar exemption applies.

- Primary Residence Exemption

If the trust property was used as a primary residence, it may qualify for the IRS capital gains exclusion, allowing up to $250,000 ($500,000 for married couples) of profit to be tax-free if lived in for at least two of the past five years. The trustee must confirm eligibility through the trust documents and verify who occupied the home. Applying this correctly can reduce tax liability and increase the amount distributed to beneficiaries.

- Inheritance and Estate Taxes

When a property in a trust passes to beneficiaries after the grantor’s death, it may be subject to inheritance or estate taxes depending on the estate’s total value. By the end of 2025, the federal estate tax exemption will be $13.99 million per individual, though several states have lower thresholds. The trustee should document the property’s step-up in basis, record it in the trust certifications, and work with a tax advisor to ensure accurate reporting and timely payment.

Legal Considerations When Selling a House in a Trust

Selling a house in a trust requires the trustee to confirm authority, follow all state laws, and fulfill their fiduciary duty to act in the beneficiaries’ best interests. The trustee must verify authority through trust certifications, secure beneficiary consent, and execute a valid Trustee’s Deed Upon Sale. Proper title transfer and documentation ensure the sale is legally compliant, transparent, and protects all parties involved.

- Authority of the Trustee

The trustee’s authority to sell a property comes from the trust documents and must be confirmed through trust certifications before listing the home. Under California Probate Code §16226, a trustee may sell real property if granted such power by the trust. This includes signing contracts, handling the title transfer, and executing a Trustee’s Deed Upon Sale. Verifying authority before entering into escrow helps prevent title issues and protects both the trustee and the beneficiaries from legal disputes.

- Beneficiary Rights

Beneficiaries have defined rights during a trust property sale, including notice, consent (if required), and access to transparent records. According to California Probate Code §16060, the trustee must keep beneficiaries reasonably informed about the trust’s administration. For example, if multiple beneficiaries disagree on the selling price or timing, the trustee must document communications and act in their collective best interest. Clear documentation and consistent updates reduce conflict and support fiduciary compliance.

- Compliance with State Laws

Selling a home held in a trust requires compliance with state and local laws on title, disclosure, and property transfer. In California, Probate Code §18100.5 lets the trustee use a Certification of Trust instead of the full document to confirm authority. Under Civil Code §1102.2(d), the trustee must still provide property disclosures to the buyer. Coordinating with an escrow company ensures all documents and funds are handled properly and the sale closes without delays.

- Fiduciary Duty

The trustee has a fiduciary duty under California Probate Code §16002 to act loyally and in the beneficiaries’ best interests. This includes selling the property at fair market value, avoiding self-dealing, and documenting all key decisions. For example, if the trustee accepts an offer below market value without proper justification, beneficiaries could claim a breach of duty. Maintaining full transparency, obtaining appraisals, and recording sale actions protect the trustee from liability and ensure the trust is administered lawfully and ethically.

5 Key Steps to Sell a Home Held in a Trust

Selling a home held in a trust involves reviewing the trust documents, consulting legal and financial advisors, selecting a qualified real estate agent, preparing the property for sale, and negotiating and finalizing the transaction. The trustee must confirm authority, comply with all state and trust laws, and coordinate with an escrow company to complete the title transfer and close the sale. Following these steps ensures a smooth, compliant, and profitable transaction for the beneficiaries.

Step 1: Review Trust Documents

The first step in selling a trust property is to verify authority and restrictions through the trust documents. These documents define the trustee’s powers, identify any beneficiary consent requirements, and outline how real property can be sold. Reviewing them early confirms that the trustee can act legally on behalf of the trust entity and helps prevent conflicts or procedural errors during the sale.

The trustee should also review the trust certifications to confirm signature validity and ensure the escrow company and title officer can recognize their authority. If the trust includes special conditions such as restrictions on price, sale timing, or notice requirements, these must be addressed before listing. A legal review at this stage avoids compliance issues and supports a smooth transaction from listing to closing.

Step 2: Consult Legal and Financial Advisors

Before proceeding with the sale, the trustee should consult a trust attorney and a Certified Public Accountant (CPA) to confirm compliance and minimize liabilities. The attorney ensures that all actions meet Probate Code requirements, including execution of the Trustee’s Deed Upon Sale and notification of beneficiaries where required. This step protects the trustee from personal liability and confirms adherence to fiduciary obligations.

A CPA or tax advisor evaluates potential capital gains tax, property tax reassessment, and possible estate tax exposure. Early tax planning ensures the sale structure benefits all beneficiaries and aligns with the trust’s financial goals. Professional guidance at this stage ensures the transaction is both compliant and financially optimized.

Step 3: Choose the Right Real Estate Agent

Choosing an agent experienced in trust and probate sales ensures compliance and efficiency throughout the selling process. The right real estate agent understands the legal nuances, including documentation such as the Certification of Trust and Trustee’s Deed Upon Sale, and can navigate buyer questions about the trust sale process.

Once the trustee selects an agent, they should review the comparative market analysis (CMA) to determine a fair listing price and discuss buyer contingencies, seller concessions, and pre-approval requirements. A skilled agent provides market insight, streamlines communication between all parties, and ensures the property is competitively positioned. This combination of legal understanding and market expertise helps protect the trust’s financial interests and the beneficiaries’ value.

Step 4: Prepare the Home for Sale

Preparing the home for sale allows the trustee to fulfill their fiduciary duty by enhancing the property’s market appeal and sale value. The trustee should coordinate repairs, deep cleaning, and light staging to make the property more attractive to potential buyers. According to the Home Staging Institute, well-staged homes sell up to 73% faster, showing that presentation directly impacts market performance.

Partnering with the real estate agent during this stage ensures the home aligns with market expectations and listing standards. Proper preparation not only strengthens buyer interest but also supports a faster, smoother sale process that maximizes returns for the trust and beneficiaries.

Step 5: Negotiate Offers and Finalize the Sale

The final step is to review and negotiate offers based on price, contingencies, and buyer qualifications. The trustee should evaluate each offer with the real estate agent, ensuring it aligns with the trust’s financial objectives and legal requirements. Strong documentation and timely communication with buyers help maintain transparency and trust.

Once an offer is accepted, the trustee works with the escrow company to handle the title transfer, confirm the trust’s authority on closing documents, and execute the Trustee’s Deed Upon Sale. After closing, proceeds are distributed according to the trust terms. This careful approach ensures compliance, protects all parties, and fulfills the trustee’s obligations efficiently.

What Are the Different Types of Trusts for Selling a House?

The primary trust structures for selling a house include revocable trusts, irrevocable trusts, testamentary trusts, and specialized trusts. Each structure defines how ownership rights, tax obligations, and trustee authority are managed during a sale. Understanding these distinctions helps the trustee handle transactions correctly, distribute proceeds lawfully, and ensure full compliance with trust and tax regulations.

Revocable Trust

A revocable trust, often called a living trust, allows the grantor to retain control of the property while they are alive. This flexibility means the grantor or trustee can modify the trust, add or remove assets, or sell the home at any time without court approval. When selling a house held in a revocable trust, the process is similar to a standard property sale, except that the trustee acts on behalf of the trust entity rather than in an individual capacity.

Because ownership remains under the grantor’s control, the trustee can coordinate directly with a real estate agent and escrow company to manage the title transfer, execute the Trustee’s Deed Upon Sale, and finalize the transaction. This structure simplifies the process, avoids probate, and ensures the sale complies with both trust terms and state real estate laws.

Can you sell a House in a Revocable Trust?

Yes, you can sell a house in a revocable trust at any time because the grantor keeps full control over the trust and its assets. The trustee manages the transaction on behalf of the trust, handling the listing, negotiation, and title transfer. This structure allows a quick, private sale without court approval and helps avoid the delays and costs of probate.

Irrevocable Trust

An irrevocable trust is a legal arrangement in which the grantor permanently transfers ownership of a property to the trust, giving full control of that asset to the trustee. This type of trust is commonly used for estate planning and asset protection, but it limits the grantor’s ability to modify terms or sell the property directly. Any sale must comply with the trust’s written terms and state laws, with the trustee overseeing approvals, documentation, and distribution of proceeds.

Selling a home in an irrevocable trust typically requires additional documentation, such as trust certifications and legal approval, to confirm authority. While this process is more restrictive than with a revocable trust, it provides tax benefits and safeguards against creditors, making it an effective long-term planning tool.

Can You Sell a House in an Irrevocable Trust Before Death?

Yes, you can sell a house in an irrevocable trust before the grantor’s death, but only if the trust documents allow it and the trustee and beneficiaries agree. Since the grantor gives up control once the trust is created, the trustee must handle the sale according to the trust’s terms and obtain necessary approvals. This ensures the sale remains valid, protects beneficiary interests, and upholds the trust’s legal purpose.

Can You Sell a House in an Irrevocable Trust After Death?

Yes, you can sell a house in an irrevocable trust after the grantor’s death, provided the trustee has authority under the trust terms. Once the grantor passes, the trust becomes the legal owner of the property, and the trustee administers the sale as part of the estate settlement. The proceeds are then distributed to the beneficiaries based on the trust’s instructions, often avoiding probate and ensuring a faster transfer of assets.

Testamentary Trust

A testamentary trust is a legal entity created through a person’s will and activated only after their death. It holds and manages the deceased’s assets, including real estate, according to the instructions in the will. When selling a house held in a testamentary trust, the trustee manages the transaction on behalf of the beneficiaries, ensuring the sale aligns with the estate’s settlement terms and local probate laws.

Because the trust forms after death, the property often goes through probate before being transferred into the trust. Once the court approves the transfer, the trustee can list and sell the property, handle the title transfer, and distribute the proceeds as directed. This structure allows the grantor to maintain control over how the property is handled after death while ensuring the beneficiaries receive their share according to the will’s instructions.

Specialized Trust

A specialized trust is designed to serve a specific legal or financial purpose beyond general estate management. When selling a house held in such a trust, the trustee must ensure the transaction aligns with the trust’s intended objective, whether it involves supporting a charitable cause, protecting a special needs beneficiary, or preserving Medicaid eligibility. Each type has distinct rules governing how property can be sold and how the proceeds must be used or retained.

- Charitable Trusts

A charitable trust holds property to benefit a recognized charity or public purpose. When the property is sold, the trustee must direct the sale proceeds to the named charity as stated in the trust documents. This structure supports philanthropy while offering potential tax advantages under IRS charitable regulations.

- Special Needs Trusts

A special needs trust provides financial support for a disabled individual without affecting government benefit eligibility. If the property is sold, the trustee must ensure proceeds remain in the trust and are used for the beneficiary’s care. This setup safeguards both assets and continued access to Medicaid or SSI benefits.

- Medicaid Irrevocable Trusts

A Medicaid irrevocable trust helps individuals qualify for Medicaid by transferring ownership of assets like a home. When selling the property, the trustee must comply with Medicaid’s five-year lookback rule and keep proceeds within the trust. Doing so preserves Medicaid eligibility and prevents disqualification due to asset transfers.

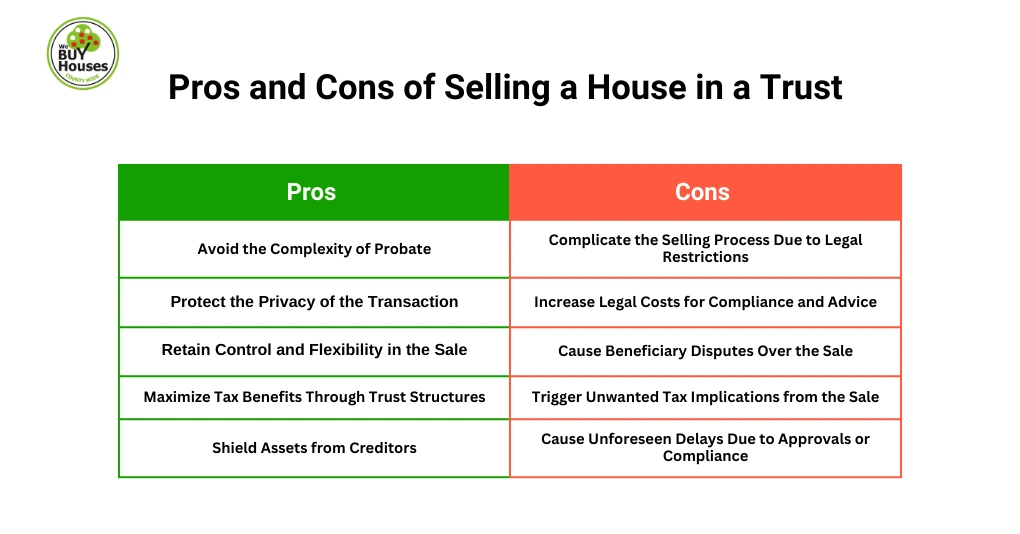

Pros and Cons of Selling a House in a Trust

Selling a house in a trust provides key benefits like probate avoidance, privacy, and tax advantages, but comes with drawbacks such as legal complexity, higher costs, and potential beneficiary disputes, making the decision a balance between convenience and required oversight. Understanding these trade-offs helps the trustee manage the sale responsibly and align each step with the trust’s legal and financial objectives.

What are the Pros of Selling a House in a Trust?

Selling a house in a trust results in probate avoidance, stronger privacy, greater control, valuable tax opportunities, and asset protection, all of which help the trustee manage the transaction efficiently while safeguarding the beneficiaries’ financial interests.

- Avoid the Complexity of Probate

A trust-based sale avoids the delays, court filings, and legal fees associated with probate. Since the property is already owned by the legal entity of the trust, the trustee can move directly to listing and closing. This faster process delivers beneficiaries quicker access to proceeds and reduces administrative burdens for everyone involved.

- Protect the Privacy of the Transaction

Trust property sales remain confidential because they do not require public probate filings. Details such as the trust documents, beneficiary identities, financial terms, and distribution amounts stay private. This protects the family’s information and prevents public scrutiny, which is especially valuable in high-value or sensitive estates.

- Retain Control and Flexibility in the Sale

The trustee maintains clear authority to manage the sale from start to finish. They can select the real estate agent, set the listing strategy, negotiate the sales price, evaluate contingencies, and manage the closing process without court supervision. This level of control ensures the sale aligns with the trust’s goals and supports the beneficiaries’ best interests.

- Maximize Tax Benefits Through Trust Structures

Trusts may provide access to tax advantages such as the primary residence exclusion or stepped-up basis, depending on how the property is held. Proper planning allows the trustee to reduce capital gains exposure, capture tax savings for the trust, and increase final distributions. These benefits often make trust-held properties more financially efficient to sell than personally owned homes.

- Shield Assets from Creditors

Certain structures, particularly irrevocable trusts, protect trust assets from creditor claims and legal judgments. When the property is sold, proceeds remain safeguarded inside the trust and can be allocated according to its terms. This protection preserves wealth for the beneficiaries and supports long-term estate planning objectives.

What are the Cons of Selling a House in a Trust?

The main cons of selling a house in a trust include extra legal procedures, higher advisory expenses, potential beneficiary conflicts, tax complications, and delays tied to compliance and approvals. These issues require the trustee to manage the process with precision to avoid legal, financial, and administrative setbacks.

- Complicate the Selling Process Due to Legal Restrictions

Trust property sales must follow the exact instructions written in the trust documents, comply with state trust laws, and include verification through trust certifications. The trustee must prove their authority before the escrow company or title officer can proceed. These added steps increase administrative work but ensure the sale is enforceable and fully aligned with the trust’s legal structure.

- Increase Legal Costs for Compliance and Advice

A trust sale typically requires guidance from a trust attorney, CPA, and sometimes a real estate attorney to ensure documents like the Trustee’s Deed Upon Sale and disclosure forms meet legal standards. These costs add up due to the specialized nature of trust transactions, yet they help prevent errors that could invalidate the sale or expose the trustee to liability.

- Cause Beneficiary Disputes Over the Sale

Beneficiaries may disagree on the listing price, whether to accept contingencies, or how proceeds should be allocated. Conflicts arise more often when multiple heirs share the property. The trustee must document decisions, explain reasoning, and follow the trust instructions to protect the sale from internal challenges and maintain fiduciary compliance.

- Trigger Unwanted Tax Implications from the Sale

Depending on the trust type, the sale may lead to capital gains tax, loss of primary residence exclusions, or reassessment consequences. For irrevocable trusts, beneficiaries may face different tax reporting obligations, and proceeds must remain in the trust. Without proper planning, these tax burdens reduce inheritance value, making early consultation with a tax advisor essential.

- Cause Unforeseen Delays Due to Approvals or Compliance

Some trust sales require beneficiary consent, court clarification, or legal review of ambiguous trust language before proceeding. Title issues may arise if prior amendments or trustee appointments are not properly recorded. These delays extend closing timelines but ensure the sale is legally sound and prevent disputes after distribution.

Final Considerations When Selling a House in a Trust

Selling a house in a trust requires confirming that all legal, tax, and beneficiary requirements are met before closing. The trustee should recheck the trust documents, confirm any necessary approvals, consult legal and tax professionals, and ensure accurate title transfer and proper fund distribution to keep the sale compliant with the trust’s terms.

If the trustee wants a quicker, low-risk option without delays tied to repairs, contingencies, or buyer financing, a reputable property investment group can provide a direct cash offer, faster closing timelines, and a simplified process. This helps the trust complete the sale efficiently while protecting the beneficiaries’ financial interests.