Yes, you can sell a house in an irrevocable trust, but it depends on the trust’s terms and the authority granted to the trustee. While the trustee generally has the authority to sell the property, they must comply with the trust document’s provisions, which may require obtaining beneficiaries’ consent or court approval. The trustee’s fiduciary duty ensures that any sale aligns with the trust’s goals and complies with legal requirements.

Although selling a house in an irrevocable trust is feasible, it is essential to carefully review the trust agreement and understand the specific terms. Trustees must fulfill their fiduciary duties and ensure beneficiaries’ rights are respected. Seeking legal counsel can help navigate the process, ensuring the sale is conducted properly and avoiding any potential complications.

What Does It Mean When a House Is in an Irrevocable Trust?

When a house is placed in an irrevocable trust, the legal ownership is permanently transferred from the original owner (the grantor) to the trust itself. This creates a protective barrier around the asset, making it useful for reducing estate taxes, shielding the property from the grantor’s personal creditors, and establishing enforceable rules for future administration.

Additionally, under a house placed in inrrevovable trust, the trustee becomes responsible for administering the house, including maintenance, tax payments, and any future sale, strictly in accordance with the trust document. However, this authority is limited by a fiduciary duty that requires the trustee to act solely in the beneficiaries’ best interests.

How Irrevocable Trusts Differ From Revocable Trusts?

Irrevocable trusts permanently transfer ownership and control of assets to the trust, whereas revocable trusts allow the grantor to retain control and freely add, remove, or dissolve assets during their lifetime. An irrevocable trust restricts control from the start, enabling asset protection and potential estate tax benefits. When selling a house in a trust, an irrevocable trust requires the trustee to follow strict terms, and any sale may require beneficiary consent or court approval.

In contrast, a revocable trust primarily functions as a probate-avoidance tool, and the grantor can modify terms or sell property without restrictions until death, at which point the trust becomes irrevocable.

Difference Between Irrevocable and Revocable Trusts

| Aspect | Irrevocable Trust | Revocable Trust |

| Ownership of assets | Owned by the trust | Controlled by the grantor |

| Ability to change terms | Generally not allowed | Allowed at any time |

| Grantor control | Relinquished or limited | Fully retained |

| Creditor protection | Often protected | Not protected |

| Estate tax impact | May reduce taxable estate | Included in taxable estate |

| Primary purpose | Asset protection and tax planning | Probate avoidance and flexibility |

Note: Even a revocable trust ultimately becomes irrevocable when the grantor loses the capacity to manage their financial affairs or passes away.

Who Actually Owns the Property?

In an irrevocable trust, the trustee holds legal ownership of the property, while the original owner, or grantor, permanently gives up control and ownership rights. As a fiduciary, the trustee must manage, maintain, or sell the property strictly in accordance with the trust document and always in the best interests of the beneficiaries. Beneficiaries do not own the house directly, but they hold a beneficial interest that entitles them to receive financial benefits from the property, such as rental income or proceeds from a future sale.

How Does Property Get Into an Irrevocable Trust?

Property gets into an irrevocable trust through a formal legal process in which the grantor transfers ownership of assets from personal ownership into the trust’s name. This can include assets like real estate, cash, or investment accounts. Once the transfer is completed, the property is no longer part of the grantor’s personal estate, and the grantor gives up direct control over the asset.

Step-by-Step Process for Transferring Property Into an Irrevocable Trust

- Property Title Transfer: The grantor prepares a new deed, whether a Quitclaim or a Warranty Deed, that officially names the trust as the owner.

- Notarize and Record: This deed is then properly signed, notarized, and recorded by the grantor with the local recording authority to make the transfer legally valid.

- Retitle Related Assets: If additional assets are being placed into the trust, an Assignment of Interest may be used to transfer bank accounts, investment accounts, or insurance policies into the trust’s name, often using the trust’s TAX ID

- Legal Review: An estate planning attorney should review the transfer documents to confirm that the deed language is correct and that the trust is properly funded in accordance with state law.

Why Ownership Matters for Selling?

Ownership matters because it determines who has the legal authority to sell a house held in an irrevocable trust and what approvals are required for the sale to proceed. In this structure, the trustee holds legal ownership and can manage or sell the property only as permitted by the trust document.

Beneficiaries, on the other hand, hold a beneficial interest, meaning they receive financial benefits from the property but do not control the sale. If the trust limits the trustee’s authority or requires beneficiary consent or court approval, the sale can be delayed or blocked. Therefore, clear ownership and defined authority help ensure that sale proceeds are processed legally without dispute.

Who Has the Authority to Sell the House in an Irrevocable Trust?

The trustee has the primary authority to sell a house in an irrevocable trust, acting as the legal owner and managing the property for the beneficiaries’ benefit. However, the trustee’s power to sell is not automatic or unlimited and depends entirely on the trust document, which may require beneficiary consent or court approval for certain actions. Additionally, if there are multiple trustees, they must act together or by majority vote, depending on the trust’s terms.

What Is the Trustee’s Legal Authority?

A trustee holds legal authority over trust property as granted by the trust document, including the power to manage and sell real estate, invest trust assets, and handle taxes. This authority must always be exercised under a strict fiduciary duty, requiring the trustee to act in the best interests of the beneficiaries and place those interests above their own. While trustees can typically sell trust property, they must comply with conditions or limitations set out in the trust, which may restrict when and how a sale can occur.

6 Core Authorities and Fiduciary Duties of a Trustee

- Asset Management: Take legal control of trust assets and manage investments such as real estate, stocks, or business interests while protecting trust property.

- Fiduciary Duty: Act with loyalty, prudence, and impartiality in all decisions affecting beneficiaries.

- Distributions: Distribute income or principal to beneficiaries strictly according to the trust’s distribution rules.

- Record Keeping: Maintain accurate financial records and provide required reports to beneficiaries.

- Tax Compliance: File trust tax returns, including IRS Form 1041, and pay trust-related taxes.

- Legal Actions: Represent the trust in legal matters, pay valid claims, and hire professionals such as attorneys or accountants when needed.

When Is Beneficiary Consent Required?

Beneficiary consent is required when the trust document limits the trustee’s authority and conditions certain actions, such as selling trust property, on beneficiary approval. This commonly applies when the trust requires unanimous or majority consent to ensure the trustee’s decision aligns with the trust’s purpose and does not harm beneficiaries.

Consent from the beneficiary is also necessary if the grantor is no longer involved due to incapacity or death and the trustee seeks to take actions not clearly authorized by the trust. If required consent cannot be obtained, the trustee typically must seek court approval before proceeding to prevent disputes or legal challenges.

When Is Court Approval Necessary?

Court approval is necessary when the trust document is unclear, the trustee’s authority to sell is uncertain, or beneficiaries disagree about the sale of trust property. It may also be required if the trustee cannot obtain the required beneficiary consent or wants confirmation that a proposed sale complies with trust law. Although seeking court approval can add time and expense, it helps protect the trustee from liability and ensures the sale is legally valid. Trustees should seek legal guidance early when disputes arise or when trust terms are ambiguous.

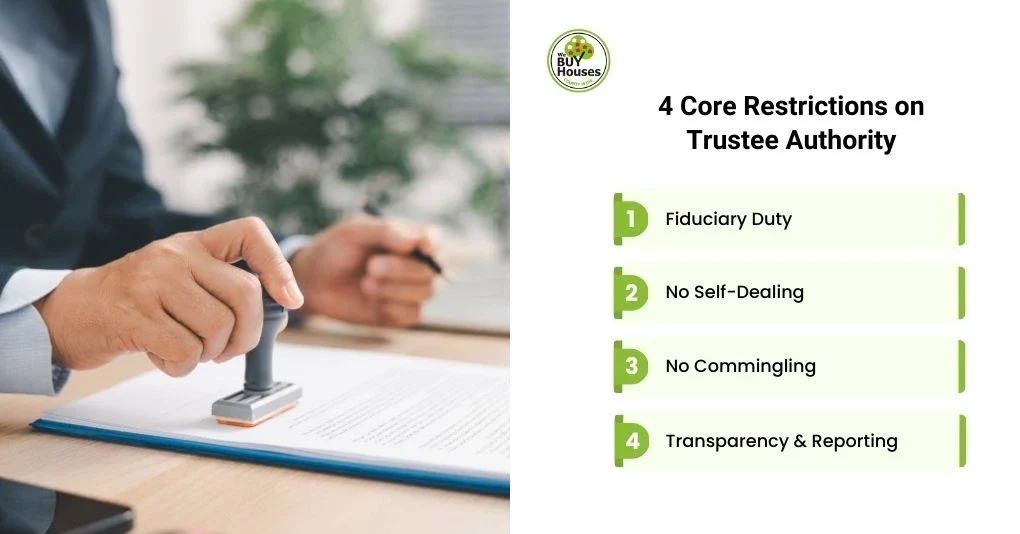

What Are the Restrictions on Trustee Authority?

The restrictions on trustee authority are defined by the trust document and fiduciary law, which prohibit self-dealing and commingling of trust assets and require transparency through proper accounting. Even when a trust grants broad powers, trustees must always comply with legal standards that prohibit conflicts of interest and improper personal benefit, especially when the trustee is also a beneficiary.

4 Core Restrictions on Trustee Authority:

- Fiduciary Duty: Trustees must act solely in the best interests of beneficiaries, prioritizing their welfare above all else.

- No Self-Dealing: Cannot personally profit from trust property or engage in prohibited transactions without consent or court approval.

- No Commingling: Must keep trust assets completely separate from personal assets.

- Transparency & Reporting: Provide beneficiaries with clear records and accurate trust accountings.

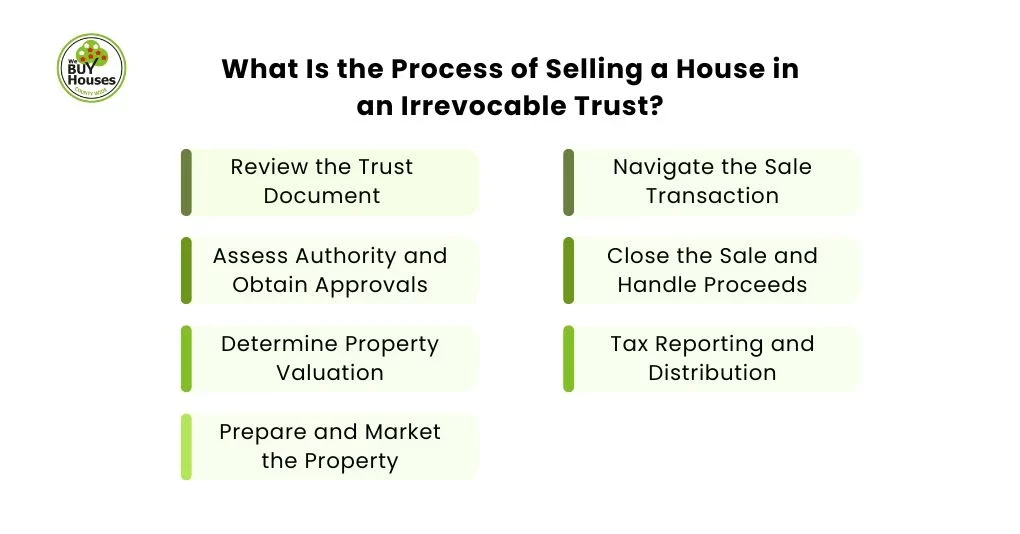

What Is the Process of Selling a House in an Irrevocable Trust?

Selling a house in an irrevocable trust involves confirming the trustee’s authority to sell, obtaining beneficiary consent or court approval if required, and determining the property’s fair market value. The trustee must also prepare and market the property, negotiate the sale, and ensure proceeds are distributed per the trust’s terms. Additionally, the trustee must handle tax obligations and ensure that the sale is legally compliant and fair to the beneficiaries.

Review the Trust Document

The first step in selling a house in an irrevocable trust is reviewing the trust agreement to confirm the trustee’s authority and identify any restrictions on the sale. The trustee must look for clauses that grant or limit the power to sell, require beneficiary consent, mandate court approval, or impose conditions on how proceeds must be handled. Additionally, the trustee must collect the Certification of Trust, the Grantor’s Death Certificate (if applicable), and the Trust’s Tax ID Number (EIN).

Assess Authority and Obtain Approvals

After reviewing the trust, the trustee must confirm whether they have full authority to sell or if additional approvals are required. Some trusts require written consent from beneficiaries, while others mandate court approval when authority is unclear or when beneficiaries disagree. Securing all required approvals before listing the property is critical to avoid delays, legal challenges, or the invalidation of the sale.

Determine Property Valuation

Determining Fair Market Value (FMV) is critical because the trustee has a fiduciary duty to sell trust property prudently. This is typically done through a professional appraisal or a comparative market analysis (CMA) of similar local sales. To fulfill this duty, the trustee can hire a licensed appraiser for a legally recognized valuation or use a CMA from a real estate agent to assess local market conditions. Selling below FMV could expose the trustee to personal liability if beneficiaries claim the trust was defrauded.

Prepare and Market the Property

After evaluating your home’s market value, list the home to attract qualified buyers and support a fair market sale. This may include completing necessary repairs, staging the home, hiring a real estate agent, and using professional photography for listings. All marketing efforts should align with the trust’s goals and the trustee’s obligation to maximize value for beneficiaries.

Navigate the Sale Transaction

Once offers are received, the trustee evaluates and negotiates terms consistent with market value and trust requirements. The trustee reviews and signs the purchase agreement, manages contingencies such as inspections or financing, and ensures all contractual terms are properly documented. Clear communication and careful oversight help ensure a smooth and legally compliant transaction.

Close the Sale and Handle Proceeds

At closing, the trustee executes final documents, transfers title, and ensures sale proceeds are properly received by the trust. Any outstanding debts, liens, or sale-related expenses must be paid before distributions occur. The trustee then handles proceeds strictly according to the trust’s distribution instructions.

Tax Reporting and Distribution

After the sale, the trustee must address tax obligations, including reporting the sale on the trust’s tax return, calculating capital gains tax, and accounting for deductions. The trustee files Form 1041 for the trust’s income and, if applicable, passes it to beneficiaries, who report it on their Form 1040. Once taxes are settled, the trustee distributes the remaining proceeds to beneficiaries as directed in the trust document, either as a lump sum or over time, while ensuring proper documentation to maintain compliance and transparency.

Selling Before vs. After the Grantor’s Death

Selling an asset in an irrevocable trust before the grantor’s death means the trust retains the original, lower basis (resulting in higher taxes), while selling after death typically triggers a stepped-up basis (lower taxes on appreciation). However, this can vary depending on the trust type (grantor or non-grantor) and IRS rules.

With recent guidance from Rev. Rul. 2023-2 suggesting that some irrevocable grantor trusts may not receive the step-up, making post-death sales more complex for tax savings. Therefore, understanding these differences ensures the sale complies with legal requirements and aligns with the trust’s goals.

Selling a House in an Irrevocable Trust Before Death

When selling a house in an irrevocable trust before the grantor’s death, the trust retains the original, lower cost basis, meaning capital gains are calculated from that basis, often resulting in higher taxable profit. While this process allows for early distribution or reinvestment, the sale may qualify for certain exclusions if the house was the grantor’s primary residence.

However, because there is no step-up in basis, the trustee must manage the sale with careful attention to tax implications, and the grantor cannot modify the terms once the property is in the trust.

Selling a House in an Irrevocable Trust After Death

After the grantor’s death, the irrevocable trust becomes fully binding, and the trustee assumes full authority to manage and sell the property according to the trust’s provisions. Traditionally, when selling an inherited house, assets in an irrevocable trust would receive a step-up in basis to their FMV at death, reducing capital gains taxes.

However, recent IRS guidance (Rev. Rul. 2023-2) states that assets in an irrevocable grantor trust do not receive a step-up in basis, which increases taxes for beneficiaries. In contrast, non-grantor trusts generally receive the step-up in basis. The trustee must manage the sale, distribute proceeds per the trust’s terms, and may need an EIN for tax reporting. If there are disputes or if the trust’s terms are unclear, court approval may be necessary.

Key Differences and Tax Advantages of Timing

Selling a property before the grantor’s death means the sale is subject to capital gains tax without the benefit of a step-up in basis, whereas selling after the grantor’s death allows for a step-up in basis, which can significantly reduce capital gains tax.

While selling before death may offer quicker flexibility, it does not provide the same tax advantages, such as reduced tax liability on appreciation, as selling after death. Therefore, trustees should carefully assess the timing and consult tax professionals to determine the best approach to minimize tax exposure and maximize benefits for beneficiaries.

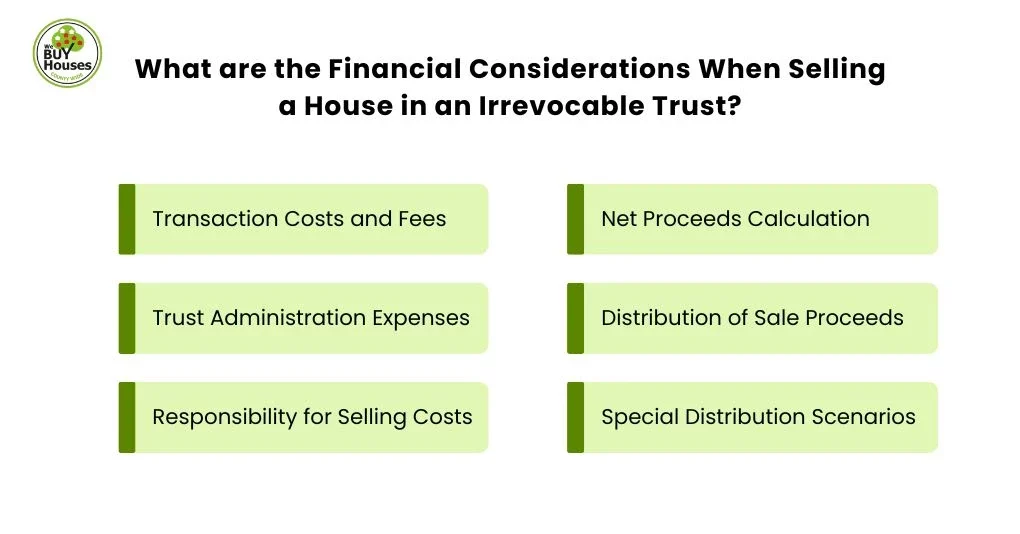

What are the Financial Considerations When Selling a House in an Irrevocable Trust?

When selling a property in an irrevocable trust, the trustee must consider transaction costs, administrative expenses, and the distribution of proceeds to beneficiaries. The trustee must ensure all costs are covered according to the trust’s terms and that proceeds are distributed fairly. In cases involving special distribution scenarios, such as with minor beneficiaries or those with special needs, additional planning and legal advice may be required to ensure compliance with the trust’s provisions.

Transaction Costs and Fees

Selling a property in an irrevocable trust incurs transaction costs such as agent commissions (typically 5-6%), closing costs, and repairs, all of which reduce the net proceeds from the sale. The trustee must ensure these expenses are properly accounted for and paid in accordance with the trust’s terms. Since these costs directly impact the funds available for distribution to beneficiaries, the trustee should also consult with professionals to confirm any negotiable fees.

Trust Administration Expenses

When selling a house in an irrevocable trust, consider trust administration expenses such as legal fees, accounting costs, and trustee compensation. These expenses are typically deducted from the trust before proceeds are distributed to beneficiaries. The trustee must ensure that all fees are transparent, justified, and in compliance with the trust’s terms to prevent unnecessary reduction of the trust estate’s value.

Responsibility for Selling Costs

The trust typically covers selling costs, including commissions, closing fees, and repairs. However, the trust document may assign some costs to beneficiaries. Trustees must ensure that the costs are covered according to the trust’s terms. If the terms are unclear, they should consult legal professionals for clarification.

Net Proceeds Calculation

Calculating the net proceeds from a house sold in an irrevocable trust involves subtracting selling expenses (such as commissions, closing costs, and improvements) from the sale price. A key difference in this calculation is the cost basis, which typically remains the original gift amount, rather than receiving a step-up to the date-of-death value. This can result in capital gains tax, which is usually paid by the trust or beneficiaries, unlike personal home sales, where exclusions may apply. After accounting for taxes and expenses, the remaining funds are distributed according to the trust’s terms.

Distribution of Sale Proceeds

After deducting selling costs and expenses, the trustee must distribute the remaining proceeds following the trust document’s terms. This may include lump sum payments or scheduled distributions, depending on the trust’s provisions. Proper documentation of the distribution process is essential to ensure transparency and avoid disputes.

Formula for calculating the Net Proceeds for Distribution:

- Net Proceeds for Distribution = Sale Price – (Basis + Improvements + Selling Costs)

For example, a house held in an irrevocable trust sells for $500,000. The original basis is $300,000, capital improvements total $50,000, and selling costs (agent fees, closing costs, taxes) are $40,000. Using the formula:

Net Proceeds for Distribution = $500,000 − ($300,000 + $50,000 + $40,000) = $110,000

In this example, $110,000 would be available for distribution to beneficiaries under the trust’s terms.

Special Distribution Scenarios

In certain cases, the sale of property in an irrevocable trust may involve special distribution scenarios, such as for minor beneficiaries, special needs trusts, or charitable interests. Trustees must carefully follow the trust document’s provisions to ensure compliance with legal requirements and protect beneficiaries’ interests, consulting legal experts when necessary.

What Are the Tax Implications of Selling a House in an Irrevocable Trust?

When selling a property in an irrevocable trust, there are several tax implications, including capital gains tax, property taxes, and tax reporting requirements that the trustee must understand. The trust estate and beneficiaries can both be affected by these tax obligations, which can influence the amount distributed to beneficiaries. Understanding these tax implications ensures the sale is compliant with legal and tax regulations and helps the trustee fulfill their responsibilities effectively.

Cost Basis and Step-Up Rules

The cost basis is the original value of the property, including any capital improvements or significant repairs. If the property was inherited, the cost basis may step up to the fair market value at the time of the grantor’s death, reducing the capital gains tax when sold. In irrevocable trusts, the cost basis often carries over, potentially resulting in higher taxes if the property has appreciated significantly. Understanding how the cost basis and step-up rules apply is crucial for determining the capital gains tax owed when selling property in the trust.

Capital Gains Tax Exposure

Capital gains tax is the tax levied on the profit made from the sale of property. It is calculated by subtracting the property’s adjusted cost basis from the sale price. In an irrevocable trust, the trust pays the capital gains tax, which can be a significant amount depending on the length of time the property has been held and its appreciation. The trustee must ensure that the sale price is aligned with the current market value and that all taxes are reported and paid correctly, which may require filing Form 1041 for the trust.

Formula to calculate capital gain tax:

- Capital Gain = Selling Price – Adjusted Cost Basis – Selling Expenses

For example, assume a property held in an irrevocable trust sells for $600,000. The adjusted cost basis is $420,000, and selling expenses total $30,000. Using the capital gain formula:

Capital Gain = $600,000 − $420,000 − $30,000 = $150,000

In this example, the trust would report a $150,000 capital gain and pay the applicable capital gains tax, as required by the IRS, on Form 1041.

Capital Gains Exclusion for Irrevocable Trusts

While individuals can use IRS Section 121 to exclude capital gains tax on the sale of their primary residence, this exclusion generally does not apply to most irrevocable trusts. However, if the property held by the trust is the primary residence of the beneficiaries and they meet the ownership and use requirements, the trust may qualify for the capital gains exclusion. This typically depends on the beneficiaries meeting the two-out-of-five-year living requirement and the property being considered their primary residence, which can ultimately help avoid or reduce capital gains tax on the sale.

Property Tax Considerations

Property taxes are based on the property’s value and must be paid up to the point of sale. The trustee is responsible for ensuring that any unpaid property taxes are paid before closing, including prorating them between the buyer and seller. Additionally, some states impose property transfer taxes when ownership changes hands, and these taxes must be factored into the sale costs.

Tax Reporting Requirements

The trustee is responsible for reporting the sale of trust property to the IRS, including filing Form 1041, which reports the trust’s income and any capital gains from the sale. The trustee must also ensure that Schedule D and Form 8949 are filed correctly to report capital gains and losses. Depending on the state, the trustee may need to file additional state-specific tax forms to ensure all taxes related to the sale are properly reported.

Tax Responsibility: Trust vs. Beneficiaries

The tax responsibilities for the sale of a property held in an irrevocable trust typically fall on the trust itself, which pays capital gains tax on the taxable profits from the sale. However, if the proceeds from the sale are distributed to beneficiaries, they may be required to report the income on their personal tax returns. The trustee must ensure that the taxes are paid correctly and that beneficiaries are informed of their tax obligations related to the sale. Consulting with a tax advisor can help the trustee navigate the complex tax rules associated with irrevocable trusts.

What Are the State-Specific Considerations When Selling Trust Property?

State-specific considerations when selling trust property include variations in trust laws, real estate regulations, and tax rules, which can impact trustee duties, property transfer taxes, and disclosure requirements. Local real estate laws may dictate escrow procedures and taxes, while state trust laws may impose unique sale conditions or require court approval. Additionally, some states have different capital gains taxes or other tax implications. Trustees must be aware of these variations and consult with local legal and real estate experts to ensure compliance with all applicable laws.

Trust Law Variations by State

Trust laws vary by state, influencing how property in an irrevocable trust is sold. While federal law sets general guidelines, state law defines the trustee’s duties, such as whether court approval is required for property sales. States like California and Florida impose stricter fiduciary duties and require judicial approval for major sales, even if the trust document permits them.

Some states, like New York, require a Notice of Proposed Action for beneficiaries to object before the sale proceeds. Additionally, over 25 states (including New York and Illinois) allow decanting, transferring assets into a new, more flexible trust if the original terms are too restrictive. Understanding these state-specific laws is essential for a smooth sale.

Real Estate Law Differences

Even if the trust permits the sale, local real estate laws vary significantly by state, influencing the sale of property in an irrevocable trust. Disclosure requirements differ, with states like Alabama having minimal rules (Caveat Emptor) and states like New York mandating detailed Property Condition Disclosure Statements. Transfer taxes, such as Florida’s Documentary Stamp Tax or Pennsylvania’s Realty Transfer Tax, also vary, and some states, such as Texas and Arizona, have no state-level transfer tax.

Additionally, title companies may require different documentation. Some states accept a Certification of Trust, and others demand a full, recorded trust agreement. Trustees must understand these local regulations to ensure compliance and avoid complications.

Local Legal Counsel Requirements

Consulting local legal counsel is vital when selling a property in an irrevocable trust due to state-specific and local legal nuances. A local attorney can provide guidance on interpreting the trust document, especially if there are ambiguous terms or unclear instructions regarding the property’s sale. Local legal counsel is also essential in resolving disputes among beneficiaries or when court approval is necessary for the sale.

Since state laws vary significantly, an attorney familiar with local regulations will ensure that the trustee complies with all legal requirements during the sale process. This consultation helps avoid legal challenges and ensures a smooth transaction.

What Are the Common Challenges When Selling a House in an Irrevocable Trust?

Selling a house in an irrevocable trust can involve challenges such as beneficiary disputes, unclear or restrictive trust documents, title and lien issues, and external market conditions. These hurdles can delay the sale and may lead to legal complications if not addressed properly. Therefore, trustees must seek expert legal and financial guidance to navigate these challenges effectively and ensure the sale proceeds smoothly.

Beneficiary Disagreements

Disputes often arise regarding the sale price, timing, or even the decision to sell. While the trustee holds the legal authority, a dissenting beneficiary can stall the process by questioning the trustee’s fiduciary duty. To resolve these issues, trustees should maintain open communication and provide beneficiaries with professional appraisals. If a stalemate occurs, formal mediation or a court instruction to sell may be necessary to resolve the conflict fairly.

Ambiguous or Restrictive Trust Documents

Unclear or overly restrictive trust documents can hinder the sale process by creating confusion about the trustee’s authority and the conditions for selling the property. Ambiguities, such as conflicting instructions or vague terms, can make it difficult to determine whether the property can be sold or how the sale should proceed. In these cases, the trustee may need to seek legal interpretation or court approval to ensure the sale complies with the trust’s provisions.

Title and Lien Issues

Title issues and liens on the property can delay the sale by creating legal complications that must be resolved before the transaction can proceed. These problems, such as disputes over ownership or unresolved liens (e.g., mortgage or tax liens), must be resolved before ownership can be transferred. A thorough title search and collaboration with a title company are essential for identifying and addressing these issues. Additionally, legal assistance may be required if the title dispute or lien resolution is complex.

Valuation Disputes

Disagreements on the property’s value often arise when beneficiaries or potential buyers have differing opinions. These differences may stem from emotional attachments or varying financial expectations. To address this, the trustee should obtain an independent appraisal or a comparative market analysis (CMA) to ensure an objective assessment of the property’s value. Open communication between beneficiaries and careful negotiation with buyers can help reach a resolution and avoid delays.

Market and Timing Challenges

The success of selling a property is significantly impacted by market conditions and timing. In a slow market, achieving a desirable sale price may be difficult, while a strong market may lead to faster sales but with heightened competition. Seasonal trends also play a role, with certain times of the year being more favorable for selling than others. Trustees should stay informed about market trends and manage beneficiaries’ expectations, considering delays if conditions are unfavorable.

What are the Alternatives to Selling a House in an Irrevocable Trust?

Alternatives to selling a house in an irrevocable trust include distributing the property to beneficiaries, leasing or renting it, utilizing a 1031 exchange, or modifying/terminating the trust. These alternative options offer flexibility based on the trust’s goals, market conditions, and beneficiaries’ needs. Trustees should carefully evaluate each alternative and consult legal and financial professionals to ensure decisions align with the trust’s terms and objectives.

Distributing Property to Beneficiaries

Instead of selling, the trustee may transfer the deed directly to beneficiaries. This avoids commissions and closing fees while honoring sentimental ties. The trustee must ensure that the distribution complies with the trust’s equity rules. If there is only one house for multiple heirs, an agreement may be needed to provide equal value through other assets, preventing future claims of favoritism or legal disputes among the beneficiaries.

Leasing or Renting the Property

Renting allows the trust to keep the asset while generating income for beneficiaries or trust expenses. This is ideal during poor market conditions or when beneficiaries prefer long-term cash flow. The trustee manages the property or hires a manager to handle tenants and maintenance. This strategy preserves ownership for future appreciation, giving the trustee flexibility to wait for a more profitable time to eventually sell the home.

1031 Exchange Options

A 1031 exchange, available under Section 1031 of the IRS code, allows a trust to defer capital gains taxes by selling a property and reinvesting the proceeds into a like-kind investment property. This strategy helps preserve equity by shifting from a residential home to a more passive investment without immediate tax liability. To qualify, the trustee must identify a replacement property within 45 days and close the transaction within 180 days. Since the trust is the legal owner, it must conduct the exchange itself.

Trust Modification or Termination

If the trust’s original terms prevent a beneficial sale, the trustee may explore modification through decanting or court orders. This allows moving assets to a newer trust with more flexible rules. Termination involves distributing all assets and closing the trust, usually when maintenance costs exceed the trust’s assets. This typically requires unanimous beneficiary consent and legal oversight to ensure the action aligns with the grantor’s original intent and state laws.

Quick Sale Solutions for Irrevocable Trust Properties

To quickly sell property in an irrevocable trust, trustees can explore options such as cash offers, auction, working with real estate investors, or leasing the property. These solutions expedite the sale but come with trade-offs in terms of price and ease. Trustees must ensure compliance with the trust’s terms and prioritize the beneficiaries’ best interests.

Key Quick Sale Solutions for Irrevocable Trust Properties:

- Cash Offers: Cash sales are fast and eliminate delays like financing contingencies, allowing for quicker closings. However, it is important to choose a reliable cash buyer to avoid complications.

- Auction Sales: Auctions offer fast sales, often within a short timeframe. While they might yield lower-than-market prices, they provide transparency and speed.

- Real Estate Investors: Investors specializing in trust properties offer quick sales with minimal requirements, though the price may be below market value.

- Leasing or Renting: If the market is unfavorable, renting the property can generate income while waiting for better conditions to sell.

When deciding on a quick sale solution, trustees must consider timing, beneficiary interests, and the trust’s terms. While expedited options like cash offers and auctions speed up the process, fiduciary duties must be upheld to ensure the sale is legally and financially fair.