Picture a homeowner in San Jose who misses several mortgage payments after a sudden medical emergency. With income disrupted and bills increasing, they fall behind, and by the fourth month, the lender records a Notice of Default (NOD). This step begins the California foreclosure timeline, starting a legal process that moves quickly and gives homeowners a limited time to act.

California follows a non-judicial foreclosure process, which usually takes place without going through the courts. Once initiated, it follows a clear sequence that includes a missed payment, a Notice of Default, a Notice of Trustee Sale (NTS), and a public auction. Eviction or post-sale action can follow shortly after. Each step is regulated by fixed legal deadlines, so timing becomes critical for homeowners trying to keep their property.

Although the process is strict, foreclosure can still be avoided. The next sections explain how California homeowners can respond with loan modifications, short sales, or urgent property sales, along with the legal, financial, and credit impacts of each stage.

What does foreclosure mean?

Foreclosure is a legal process where a lender takes back a property after the borrower misses mortgage payments. It allows the lender to recover the unpaid loan balance by selling the home. In California, foreclosure is typically non-judicial, meaning it proceeds without court involvement if the loan includes a power-of-sale clause. This makes the process move faster once payments are missed.

Typically, foreclosure begins when a borrower defaults by missing three or more consecutive payments. The lender assigns a trustee to carry out legal steps, including filing a Notice of Default and scheduling a trustee sale. It is different from pre-foreclosure, which is the window before the home is taken. During this time, the borrower may still sell the home, reinstate the loan, or pursue options like a deed in lieu.

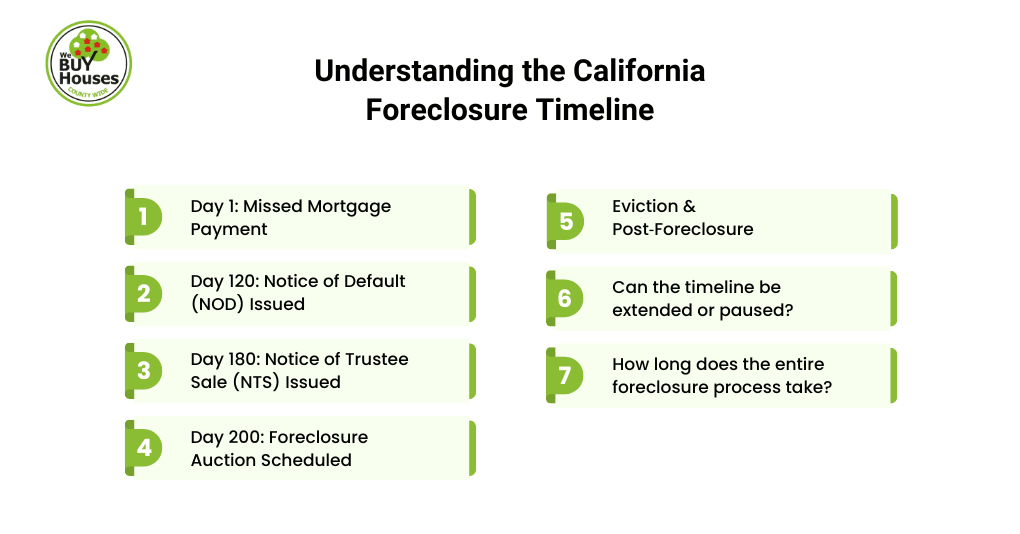

Understanding the California Foreclosure Timeline

In California, foreclosure generally spans 200 days or more and includes five key stages, such as missed payment, Notice of Default, Notice of Trustee Sale, foreclosure auction, and eviction. The process begins after a borrower misses a payment. While the timeline is structured, homeowners may still delay or stop foreclosure by modifying the loan, negotiating a sale, or filing for bankruptcy.

Day 1: Missed Mortgage Payment

A missed mortgage payment occurs when the due date passes without full payment, and the grace period, typically around 15 days, also expires. Once a payment is 30 days late, the loan is considered delinquent. At this point, lenders may apply late fees, report the missed payment to credit bureaus, and begin monitoring the account for continued risk. This marks the first formal sign of financial trouble for the borrower.

Lenders often reach out to discuss repayment options or determine the cause of delinquency. If no resolution is reached, and payments remain unpaid for three to four months, the loan may move to the foreclosure department. Acting early during this stage can prevent escalation. If the account stays delinquent, the next official step is the Notice of Default.

Day 120: Notice of Default (NOD) Issued

The Notice of Default (NOD) is the first formal legal step in the foreclosure under California Civil Code §2924. It is recorded by the trustee once the borrower is at least 90 days behind on payments and no resolution has been reached. This notice informs the borrower that they are officially in default and that the lender may proceed with foreclosure if the debt is not resolved.

After the NOD is recorded, a 90-day reinstatement period begins. During this time, the borrower can stop the foreclosure by paying the overdue amount, resolving disputes, or negotiating alternatives like a loan modification. This phase offers a final chance to retain the property. If the borrower takes no action, the process advances to the Notice of Trustee Sale, which schedules the property for auction.

Day 180: Notice of Trustee Sale (NTS) Issued

The Notice of Trustee Sale (NTS) triggers when the borrower does not cure the default during the 90 days following the NOD. It officially schedules the foreclosure auction, stating the exact date, time, and location of the sale. The NTS marks the point where the risk of losing the home becomes immediate.

By law, the NTS must be recorded at the county level and delivered at least 20 days before the sale. It must also be mailed to the borrower, posted on the property, and published in a local newspaper. While the home can still be saved, reinstatement must occur at least five business days before the auction.

This notice often prompts urgent decisions, such as negotiating a short sale or selling to a cash buyer to avoid further legal and credit consequences.

Day 200: Foreclosure Auction Scheduled

If the borrower does not reinstate the loan before the deadline, the property moves to foreclosure auction, typically scheduled around Day 200 or later. The auction is conducted by the trustee and may occur in person at the county courthouse or online, depending on the county’s procedures. The property is sold to the highest bidder, starting at the amount owed, including late fees and legal costs.

Anyone can bid at the auction, but buyers are usually required to pay in cash or certified funds at the time of sale. If no third party purchases the property, it reverts to the lender and becomes real estate owned (REO). This step ends the legal foreclosure timeline and transfers ownership. If the home is still occupied, the new owner may begin eviction proceedings shortly after the sale.

Eviction & Post‑Foreclosure

After the auction is complete, legal ownership transfers immediately to the winning bidder or back to the lender if no bids were made. Once ownership changes, any remaining occupants, whether owners or tenants, may receive a three-day notice to quit as the first step in the eviction process.

If the occupants do not leave voluntarily, the new owner can file an unlawful detainer lawsuit. In some cases, the owner may offer a cash-for-keys agreement to encourage a quicker, peaceful move-out. If that fails, the sheriff may carry out a formal eviction.

Occupants still have rights, including proper notice and, in some cases, relocation assistance. The entire eviction process usually takes 2 to 4 weeks. Around this time, the foreclosure also appears on the borrower’s credit report, impacting their score and future borrowing ability.

Can the timeline be extended or paused?

The California foreclosure timeline can pause temporarily under specific conditions, such as active loan modification review, bankruptcy protection, or litigation involving the property or lender. These situations can legally halt or delay the process, depending on the protections in place.

Other pause mechanisms include a forbearance agreement or a formal request to postpone the trustee sale, though these are typically granted at the lender’s discretion, not by obligation. It is important to note that delays rarely stop the accumulation of interest, late fees, or credit damage. Homeowners considering this route should seek legal or housing advice early, as delay options are limited and often time-sensitive.

How long does the entire foreclosure process take?

In California, a typical non-judicial foreclosure takes about 120 to 200 days from the Notice of Default to the foreclosure sale. The process moves faster than in judicial foreclosure states because it bypasses court approval.

However, the timeline can stretch if the borrower seeks delays or the lender slows action. Common causes include loan modification reviews, bankruptcy filings, legal disputes, or state-level policies like COVID-era moratoriums. While most foreclosures conclude within six to seven months, more complex cases may take longer. For a clearer estimate based on your situation, it is best to consult a HUD-approved housing counselor or foreclosure attorney.

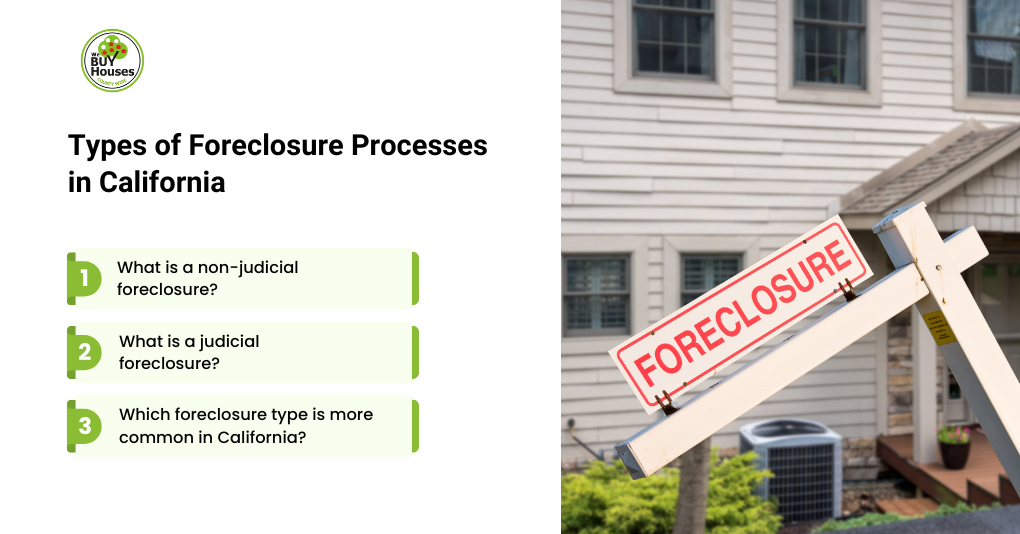

Types of Foreclosure Processes in California

California has two types of foreclosure: non-judicial and judicial. Most foreclosures in the state are non-judicial, meaning they happen without court involvement when the loan includes a power-of-sale clause. This process is faster and less costly for lenders. Judicial foreclosure requires the lender to sue the borrower in court and is typically used for loans without that clause or when pursuing a deficiency judgment.

What is a non-judicial foreclosure?

A non-judicial foreclosure is a legal process that lets a lender foreclose without going to court if the loan has a ‘power-of-sale’ clause in the deed of trust. This is the standard process in California and is governed by Civil Code §2924, which outlines the required legal steps and timeline. The process includes three main legal steps:

- Notice of Default (NOD): Filed when the borrower is at least 90 days behind on payments.

- Notice of Trustee Sale (NTS): Issued after the NOD period ends, setting the auction date.

- Foreclosure Auction: The property is sold at public auction to the highest bidder.

The full timeline typically lasts 120 to 200 days, depending on how the lender proceeds and whether the borrower responds. Non-judicial foreclosure is widely used because it is faster, less expensive, and more predictable. However, it provides limited legal protection for homeowners compared to court-supervised foreclosure.

What is a judicial foreclosure?

A judicial foreclosure is a legal process where a lender uses the court system to recover unpaid mortgage debt and authorize the sale of the property. It begins when the lender files a lawsuit in the California Superior Court.

The judicial foreclosure process in California includes the following steps:

- Complaint: The lender files a formal lawsuit against the borrower.

- Borrower Response: The borrower may respond or contest the case.

- Judgment: The court issues a decision in favor of the lender.

- Order of Sale: The court authorizes the property to be sold.

Judicial foreclosure often takes six to twelve months or more, with added court costs and public notice requirements. While uncommon in California, it allows for a deficiency judgment and provides the borrower a redemption period after the sale.

Which foreclosure type is more common in California?

Non-judicial foreclosure is by far the most common type in California, accounting for the vast majority of foreclosure cases. This is primarily because most home loans in the state include a power-of-sale clause, which allows lenders to foreclose without court involvement. As a result, the non-judicial process is generally faster, less expensive, and more predictable. Although judicial foreclosure remains legally available, lenders rarely use it due to the added time, higher legal costs, and procedural complexity involved.

Foreclosure Prevention Options for Homeowners

Homeowners in California may prevent foreclosure by pursuing options such as loan modification, short sale, deed in lieu of foreclosure, or selling the property to a cash buyer. These alternatives are often available even after a Notice of Default is filed. Acting early improves the chance of success and helps avoid auction, eviction, and long-term credit damage.

Loan Modification

Borrowers facing foreclosure may request a loan modification to adjust their mortgage terms and avoid losing their home. This option is designed to make monthly payments more affordable by reducing the interest rate, extending the loan term, or restructuring missed payments. To qualify, borrowers must demonstrate financial hardship and submit income and expense documentation. While a modification does not eliminate the debt, it can pause or stop the foreclosure process if approved. Starting early improves the chance of approval before a trustee sale is scheduled.

Short Sale

When a homeowner owes more on the mortgage than the home is worth, a short sale may offer a way to avoid foreclosure. In this process, the property is sold for less than the loan balance, and the lender agrees to accept the reduced amount as full settlement. To qualify, the borrower must show financial hardship and submit the buyer’s offer for lender approval. Although a short sale affects credit, it typically results in less long-term impact than foreclosure and allows for a more controlled exit.

Deed in lieu of Foreclosure

If foreclosure cannot be avoided through a sale or modification, a deed in lieu of foreclosure may offer a last-resort solution. In this arrangement, the homeowner voluntarily transfers ownership of the property to the lender to settle the outstanding mortgage debt. The lender must agree to the terms, and the home typically needs to be vacant and free of junior liens. Although it still impacts the borrower’s credit, this option avoids the legal and public process of foreclosure and may include debt relief or relocation support.

Selling to a Cash Buyer

For homeowners facing foreclosure, selling to a cash buyer can provide a fast and practical way to avoid an auction. Cash buyers typically purchase properties in as-is condition, meaning no repairs, inspections, or agent involvement are required. These sales can often close within 7 to 10 days, making them ideal for urgent situations. While the offer may be below market value, it provides a guaranteed outcome and immediate debt relief. This option is most effective when pursued before the foreclosure timeline reaches the auction stage.

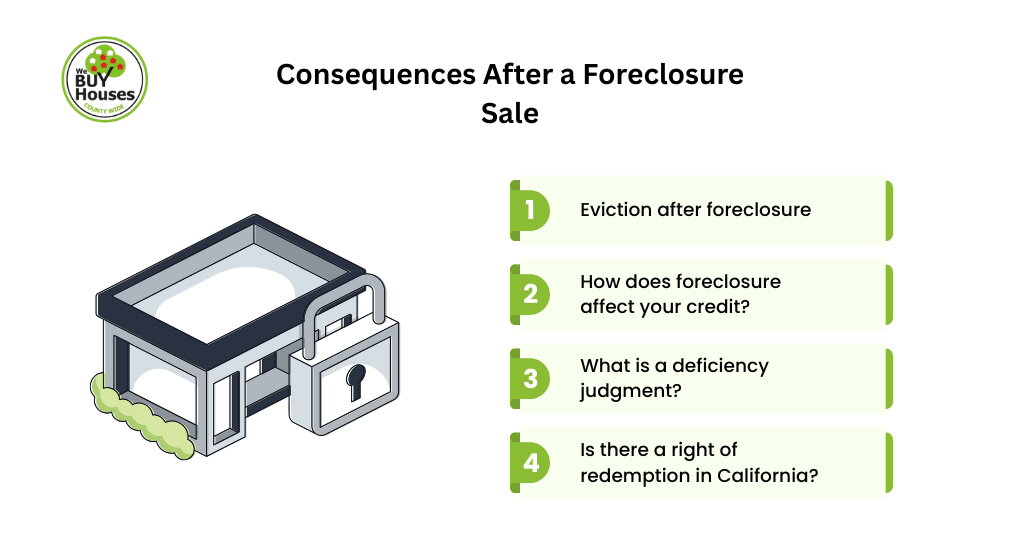

Consequences After a Foreclosure Sale

After a foreclosure sale, the homeowner loses ownership of the property, and any remaining occupants may face eviction within weeks. The foreclosure is reported to credit bureaus, typically dropping the borrower’s credit score by 100 to 160 points. In some cases, the lender may also pursue a deficiency judgment. The financial and legal impacts can last for years, especially if no resolution is reached before the auction.

Eviction after foreclosure

Eviction typically begins immediately after the foreclosure auction if the home is still occupied. The new owner must first issue a three-day notice to quit, giving the occupant time to leave voluntarily. If the occupant remains, the owner may file an unlawful detainer lawsuit, which can lead to court-ordered removal. In some cases, a cash-for-keys agreement is offered to avoid formal eviction. Most evictions occur within two to four weeks, with some differences in the process for former owners vs. tenants.

How does foreclosure affect your credit?

Foreclosure can deduct a borrower’s credit score by 100 to 160 points, depending on their credit history and profile. It is classified as a serious delinquency and stays on the credit report for seven years from the date of the first missed payment that led to foreclosure. This can affect the borrower’s ability to qualify for loans, rent housing, or get favorable interest rates. Recovery is possible, but it requires time, consistent payments, and careful credit rebuilding.

What is a deficiency judgment?

A deficiency judgment is a court decision requiring the borrower to pay the remaining loan balance if a foreclosure sale does not cover the full debt.

In California, most non-judicial foreclosures involving purchase money loans are protected by anti-deficiency laws, so lenders cannot collect the difference. However, these protections do not apply in judicial foreclosures, or when the loan was refinanced or is a second mortgage. For example, a homeowner who defaulted on a home equity loan could still be held responsible for the shortfall. Because these rules can vary by situation, homeowners need to consult a legal professional.

Is there a right of redemption in California?

A right of redemption in California exists only in judicial foreclosures, allowing the borrower to reclaim the property by repaying the full debt after the foreclosure sale. This period can last up to one year, depending on whether a deficiency judgment is pursued.

However, non-judicial foreclosures, which make up the majority of cases in the state, offer no redemption period. Once the property is sold at auction, the borrower permanently loses ownership. Knowing your foreclosure type is key to understanding your legal options.

Legal and Credit Impacts of Foreclosure in California

A foreclosure in California results in loss of ownership, negative credit reporting for up to seven years, and possible legal consequences depending on how the foreclosure was handled. These impacts can limit a borrower’s ability to secure housing, loans, or legal remedies in the future.

Key legal and credit impacts of foreclosure in California include:

- Credit Reporting: Foreclosure stays on your credit report for seven years from the first missed payment.

- Credit Score Impact: Scores may drop by 100 to 160 points, affecting future financing.

- Loan Requalification: Borrowers may be ineligible for new loans for up to 7 years, depending on loan type.

- Legal Exposure: Some borrowers may face deficiency judgments or eviction proceedings.

- Statutory Governance: California Civil Code §§2924–2924k regulates notice, timeline, and homeowner protections.

How long does a foreclosure stay on your credit report?

Foreclosure stays on your credit report for seven years from the date of the first missed mortgage payment that led to the foreclosure. It is classified as a serious delinquency, which can significantly lower your credit score and affect your ability to qualify for future loans, rent housing, or secure favorable interest rates. Although the record drops off after seven years, full credit recovery may take longer without consistent on-time payments and responsible financial behavior during the rebuilding period.

Can I get a loan after foreclosure?

You can get a mortgage after foreclosure, but you will typically need to wait 2 to 7 years, depending on the type of loan. FHA and VA loans often allow reapplication in 2 to 3 years, while conventional lenders may require 4 to 7 years with reestablished credit. During this period, maintaining a clean payment record, reducing debt, and improving your credit score are critical steps. Lenders also consider employment history and overall financial recovery before approving a new mortgage.

What are California’s foreclosure laws?

California follows a non-judicial foreclosure process in most cases, regulated by Civil Code §§2924–2924k, which outlines how lenders must legally proceed before selling a home. These laws protect homeowners through structured notice periods and procedural safeguards.

Key legal requirements include:

- Notice of Default (NOD): Must be recorded after at least 120 days of delinquency.

- Reinstatement Period: Borrowers have 90 days to cure the default.

- Notice of Trustee Sale (NTS): Must be issued at least 20 days before auction.

- No dual tracking: Foreclosure pauses during active loan modification review.

Do I need a foreclosure attorney?

You may not need an attorney in every foreclosure case, but legal help is essential when your situation involves disputes, errors, or financial complexity. A foreclosure lawyer can review notices, spot violations, and guide you through your best options.

You should consider hiring an attorney if:

- You received incorrect or missing notices

- The lender violated California foreclosure laws

- You want to challenge the process in court

- You are negotiating a short sale or loan modification

- You have filed for bankruptcy

- You suspect predatory lending

Cost and Purchase Considerations in Foreclosure

Whether you’re buying a foreclosure or selling one under financial pressure, understanding the full cost structure is crucial. These transactions often involve more than just the sale price, and hidden expenses can affect timelines, risk, and profit margins. In California, foreclosed properties tend to sell at a discount, but the purchase process and seller obligations can vary depending on the stage of foreclosure and type of sale.

Here are key financial considerations to keep in mind:

- Discounted prices due to as-is condition or urgency

- Cash payment required at auction in most cases

- Financing allowed for bank-owned (REO) properties

- Repair and inspection costs often fall on buyers

- Seller expenses may include back payments, legal fees, and closing costs

How much do foreclosure homes cost in California?

Foreclosure homes in California typically sell for 20% to 30% below market value, depending on location, property condition, and the stage of foreclosure. These properties are often priced to move quickly, especially at auction or in distressed sales.

Factors that influence the pricing of foreclosure homes in California include:

- Location: Urban areas like Los Angeles may see tighter margins

- Property condition: Poor upkeep often reduces sale value

- Stage of foreclosure: Pre-foreclosure homes may sell closer to market value

- Buyer demand: Competitive bidding can raise final prices

Do I need to pay cash to buy a foreclosure?

Yes, cash or certified funds are usually required for auction purchases, and buyers must pay the full amount within 24 to 48 hours of the sale. However, not all foreclosure sales require cash.

Here is a breakdown of common scenarios:

- Trustee auctions mandate immediate full payment via cash or certified check

- Bank-owned (REO) homes may allow conventional, FHA, or VA financing

- Hard money loans can help buyers meet fast closing requirements

- Pre-foreclosure sales often permit traditional mortgage financing

Cash buyers should prepare funds in advance and confirm payment terms. If full cash is not available, alternatives like hard money loans or bridge loans can help secure fast funding.

Can I get a mortgage on a foreclosed property?

Yes, you can finance foreclosed properties, especially bank-owned (REO) and pre-foreclosure homes listed on the market. These properties are often eligible for standard mortgage loans, provided they meet lender requirements.

Common financing options include:

- FHA loans with low down payments

- VA loans for eligible veterans

- 203k renovation loans for homes needing repairs

Homeowners should know that poor property conditions can disqualify a home from traditional financing. Lenders may require the home to be livable and insurable. For best results, get pre-approved and schedule a professional inspection before committing to a purchase.

What are the total costs when selling during foreclosure?

When selling a home during foreclosure in California, homeowners often face a combination of costs, including missed mortgage payments, legal fees, and transaction expenses. These may include mortgage arrears, accumulated late fees, foreclosure-related attorney charges, and unpaid property taxes or liens. Sellers using an agent will also need to account for standard commissions and closing costs.

The total expense varies based on the sale method. In a short sale, the lender may absorb some costs, but approval can take time, while a cash sale can close quickly and avoid agent fees, but at a lower price. Timing, urgency, and net proceeds all shape the right decision.

Foreclosure FAQs and General Concepts

What is a pre-foreclosure home?

A pre-foreclosure home is a property where the owner has defaulted on mortgage payments but the home has not yet been sold at auction. In California, this begins after the Notice of Default is recorded and continues until the foreclosure sale. During this time, the homeowner may still avoid foreclosure by reinstating the loan, refinancing, or selling the property.

Can I still live in my house during foreclosure?

Yes, homeowners can legally remain in the property during the entire foreclosure process until it is sold and the new owner completes the legal eviction process. In most cases, this means you can stay in the home through the auction date and even for several weeks afterward, depending on local eviction proceedings and negotiations like “cash for keys.”

Do I get any money if my home is foreclosed?

You may receive surplus funds if your foreclosed home sells for more than the total debt owed, including fees and liens. These excess proceeds are held by the trustee or the county, and you can file a claim to retrieve them. However, if the sale price is less than the outstanding balance, no surplus is available.