Selling a house with a mortgage is a standard process for many homeowners, as most properties are financed through loans. The sale proceeds pay off the mortgage, and if the sale price exceeds the loan balance, you keep the difference as profit. However, if the sale price is lower than what you owe, you may face negative equity, requiring a short sale or additional funds to close.

To sell a house with a mortgage, obtain a payoff statement from your lender, and estimate your home’s market value. Factor in closing costs, agent commissions, and other expenses to calculate your net proceeds. The title company ensures the mortgage is paid off and the title is cleared before transferring ownership.

Financial outcomes of selling a house with a mortgage depend on whether you have positive or negative equity. Positive equity allows for profit after paying off the mortgage and covering costs, while negative equity limits options. Tax implications, such as capital gains and depreciation recapture, can also affect your final proceeds. Understanding these factors will help you navigate the sale process and plan accordingly.

Can You Sell a House with a Mortgage?

Yes, you can sell a house with a mortgage, and it is a standard part of the home-selling process for many homeowners. In fact, 61.2% of owner-occupied homes in the U.S. have a mortgage, as reported in the Latest ACS 5-Year Estimates Data Profiles by NAR, meaning that most people will need to navigate selling with an active loan. The reason this is possible is that the mortgage does not stop the sale itself. Instead, the proceeds from the sale are used to pay off the remaining loan balance at closing, which is a standard part of the process.

When you sell a home with a mortgage, the lender receives the payoff amount from the sale proceeds. If the sale price exceeds the mortgage balance, you keep the difference as profit. However, if the sale price is less than what you owe, you may face negative equity and need to consider options like a short sale or bringing additional funds to close.

Selling with a mortgage is an ordinary process for homeowners, but understanding your mortgage balance, closing costs, and equity is essential. For instance, real estate agent commissions typically range from 5-6%, and closing costs are about 2-5% of the sale price, which will impact your final net proceeds. Knowing these factors helps you confidently navigate the sale process and know what to expect financially.

What Happens to a Mortgage When You Sell a House?

When you sell a house with a mortgage, the sale proceeds are used to pay off the mortgage, including principal, interest, and fees. The mortgage payoff statement from your lender will show the amount needed to clear the loan. Once the mortgage is fully paid, the lender issues a mortgage discharge, which releases the lien on the property, allowing the title to transfer to the buyer.

If your home sells for more than the mortgage balance, you keep the difference as profit. However, if the sale price is lower than what you owe, you may be underwater and need to consider a short sale. Remember that closing costs, like agent commissions, taxes, and title insurance, will also reduce your final proceeds.

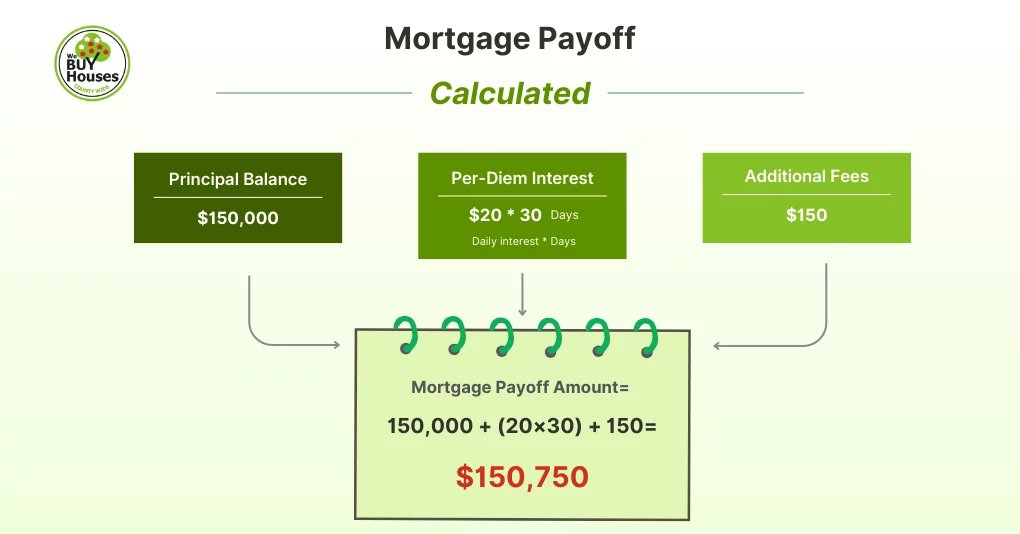

How Are Mortgage Payoff Amounts Calculated?

Mortgage payoff amounts are calculated by adding the principal balance, any per-diem interest, and additional fees. To calculate the exact mortgage payoff, the lender provides a payoff statement that includes the following:

- Principal Balance: The remaining amount of the loan you owe.

- Per-Diem Interest: Interest that accrues on the loan each day, calculated from the payoff date to the closing date.

Formula to Calculate Mortgage Payoff:

Mortgage Payoff Amount = Principal Balance + (Per-Diem Interest × Number of Days to Payoff Date) + Additional Fees

Let’s assume the following:

- Principal Balance: $150,000

- Per-Diem Interest: $20 (this is the daily interest cost based on the interest rate of the mortgage)

- Days to Payoff Date: 30 days

- Additional Fees: $150 (for processing and administrative fees)

Mortgage Payoff Amount = 150,000 + (20×30) + 150 = 150,000 + 600 + 150 = 150,750

So, the mortgage payoff amount would be $150,750. This is the amount that must be paid at closing to fully satisfy the mortgage and release the lien on the property.

Outstanding Mortgage Balance vs. Actual Payoff

The outstanding mortgage balance is the amount remaining on your mortgage, while the actual payoff is the total amount required to fully settle the loan, including any per-diem interest and additional fees. The actual payoff is always higher than the outstanding mortgage balance due to daily interest accrual and any additional charges.

| Aspect | Outstanding Mortgage Balance | Actual Payoff |

| Principal Balance | The remaining loan amount. (eg. $200,000) | Same as principal, plus interest and fees. (eg. $200,000) |

| Per-Diem Interest | Not included. ($0) | Included, based on daily interest since your last payment. (eg. $375) |

| Additional Fees | Not included. ($0) | May include administrative fees or late charges. (eg. $100) |

| Total Amount Due | The balance of the mortgage as shown on the statement. (Final: $200,000) | The total required to settle the mortgage. (Final: $200,475) |

How Does Your Home Equity Affect Your Selling Options?

Your home equity determines how much money you will walk away with after selling your home, and it significantly impacts your selling options. Positive or high equity means your home is worth more than your mortgage balance, allowing you to keep the profit after paying off the loan. However, with negative or low equity, where the mortgage exceeds your home’s value, you may need to consider a short sale or bring extra cash to close.

Having positive equity allows you to cover closing costs, which typically range from 2-5% of the sale price, and still make a profit. Negative equity, however, limits your options, requiring lender approval for a short sale or additional funds to settle the debt.

What Happens When You Sell a House Before the Mortgage Is Paid Off?

When you sell a house with an existing mortgage, the sale proceeds are first paid to cover the mortgage balance. If the sale price after adding the principal, per-diem interest, and other fees is more than the mortgage balance, you keep the difference as profit. In contrast, if the sale price is lower than what you owe, you may need to cover the shortfall by forcing a short sale or adding required funds to settle the debt. The title company will ensure the mortgage is paid in full before transferring the property title to the buyer, clearing the lien on your property.

When Do You Stop Paying Your Mortgage When Selling?

You stop paying your mortgage once the sale is finalized and the loan is paid off at closing. Until the payoff date, you are still responsible for making your regular mortgage payments. The payoff statement from your mortgage lender will outline the total amount due required to satisfy the loan, including prorated interest up to the closing date. After the sale proceeds pay off the mortgage, the lender will issue a mortgage discharge and clear the lien on the property. Be aware of the grace period deadline (usually 15 days), as missing a payment could result in additional late fees or complicate the closing. It is crucial to continue making timely payments until the mortgage is fully satisfied to ensure a smooth transaction.

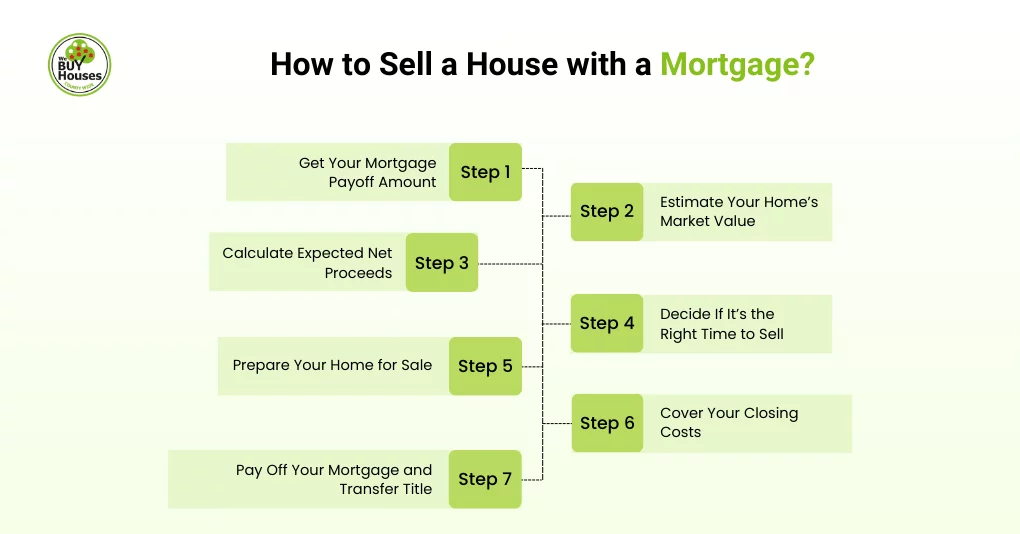

How to Sell a House with a Mortgage?

To sell a house with a mortgage, obtain a payoff statement from your lender, estimate your home’s market value, calculate net proceeds, and prepare your house for sale. Use the sale proceeds to pay off the mortgage, and if there is any remaining equity, it will be yours after closing costs are deducted. Using a structured process ensures you accurately understand the payoff amount, including principal, interest, and any additional fees, leading to a smoother transaction and minimizing surprises at closing.

7 steps for selling a house with a mortgage are:

Step 1: Get Your Mortgage Payoff Amount

The first step in selling a house with a mortgage is obtaining your mortgage payoff amount, which is the total you owe to settle the loan. Request a payoff statement from your lender, which includes the principal balance, accrued interest, and any fees like prepayment penalties if you are paying off the mortgage early. For example, if your mortgage statement shows a balance of $200,000, with $500 in interest and a $100 processing fee, the total payoff would be $200,600.

Keep in mind that the payoff statement has a limited validity period of 10 to 30 days, so request it close to your closing date. Additionally, if you have HELOCs, tax liens, or mechanic’s liens, those must be settled before transferring title to the buyer.

Step 2: Estimate Your Home’s Market Value

The next step is to estimate your home’s market value, which will help determine your equity and what you can expect after paying off your mortgage. You can do this by getting a professional home appraisal or a comparative market analysis (CMA) from a real estate agent. Understanding your home’s value is key to knowing whether you have positive equity or are underwater. For example, if your home is worth $250,000 and your mortgage payoff is $200,600, you have positive equity of $49,400. This step gives you a clear picture of your financial situation, helping you prepare for closing costs and ensuring you are ready for the sale.

Step 3: Calculate Expected Net Proceeds

After determining your home’s market value and mortgage payoff amount, calculate the expected net proceeds to assess whether you need to add extra funds or will make a profit. Subtract the mortgage payoff, closing costs (typically 2-5% of the sale price), real estate agent commission (5-6%), and any additional expenses like repairs, upgrades, staging, and marketing from the sale price. For example, if your home sells for $250,000, you owe $200,600 on the mortgage, and you incur $20,000 in closing costs and other expenses, your net proceeds would be around $29,400.

If you are selling as a For Sale By Owner (FSBO), you can save on agent commissions, but you will still need to account for advertising and legal fees. Regardless of your selling method, calculating all these expenses ensures you have a clear financial picture and can plan accordingly.

Step 4: Decide If It’s the Right Time to Sell

Deciding when to sell your home with a mortgage involves considering factors like market conditions, your home equity, and your financial goals. If you have positive equity and the market is favorable, selling sooner can help you take advantage of high demand. However, if you are underwater or the market is declining, it may be better to wait or explore a short sale.

Likewise, if you are planning to buy another home, selling before purchasing allows you to avoid carrying two mortgages, while selling and buying simultaneously requires careful planning around market volatility and closing dates. By carefully evaluating your home equity, market conditions, and personal timeline, you can make a well-informed decision about the best time to sell a house.

Step 5: Prepare Your Home for Sale

Preparing your home for sale is crucial when selling a house with a mortgage, as it can maximize the sale price and help cover your mortgage payoff. Start by making any necessary repairs or upgrades, such as fixing leaky faucets, repainting rooms, or updating fixtures, to improve the home’s condition and appeal. Staging the home can also help buyers envision themselves living there, and a NAR report reveals that staging increases the home’s value by 1-5%, which can be important when selling to ensure enough proceeds to cover your mortgage balance. If you are working with a real estate agent, they can offer guidance on which improvements will provide the best return on investment. Proper preparation will ensure your home shows well, sells faster, and potentially generates higher proceeds to pay off your mortgage.

Step 6: Cover Your Closing Costs

When selling a house with a mortgage, it is essential to factor in closing costs, which typically range from 2-5% of the sale price, excluding the real estate agent commission (usually 5-6%). These costs include title insurance (0.5%-1%), transfer taxes (0.1%-2%), and other administrative fees. For example, on a $250,000 sale, closing costs could be between $5,000 and $12,500, not including the agent’s commission. If your equity is not enough to cover both the mortgage payoff and these costs, you may need to consider options like a short sale or bring additional funds to closing. Understanding and planning these closing costs and expenses are crucial for setting realistic expectations and ensuring you are financially prepared for the sale.

Step 7: Pay Off Your Mortgage and Transfer Title

The final step in selling a house with a mortgage is paying off the mortgage at closing and transferring the title to the buyer. The payoff amount will be sent to your mortgage lender from the sale proceeds, clearing the lien on the property. Once the mortgage is paid, the title company will handle the transfer of ownership to the buyer. Any other liens, such as HELOCs or mechanics’ liens, must also be paid off before the title can be transferred. This ensures the mortgage is fully discharged, and you will receive any remaining funds after all obligations are settled.

What Financial Outcomes Should You Expect When Selling a Home with a Mortgage?

When selling a home with a mortgage, you can expect financial outcomes based on the difference between the sale price, your mortgage payoff, and any associated selling costs. If you have positive equity, you will keep the proceeds as profit after paying off the mortgage and covering costs. However, if you are underwater, you may need to cover the shortfall through a short sale or bring additional funds to closing, incurring a loss.

How Much Profit Will You Make?

If your home sells for more than the mortgage balance, your profit is calculated by subtracting the mortgage payoff amount, closing costs, and any other selling expenses from the sale price. The formula for calculating profit is:

Profit = Sale Price − Mortgage Payoff − Closing Costs − Other Expenses

For example, if your home sells for $250,000, you owe $200,000 on the mortgage, and closing costs and repairs total $15,000, your profit would be $35,000. However, if the sale price is lower than what you owe, you may need to explore options like a short sale or bring additional funds to closing. Understanding these calculations ensures you are prepared for your financial outcome.

How Do Closing Costs Affect Your Net Proceeds?

Closing costs can significantly reduce your net proceeds when selling a home with a mortgage. These costs, ranging from 6-10% of the sale price, include agent commissions (5-6%), title insurance (0.5%-1%), transfer taxes (0.1%-2%), and other administrative fees. For example, if your home sells for $250,000, and your closing costs amount to 9% of the sale price ($22,500), this will be deducted from your final proceeds after paying off the mortgage. It is important to account for these costs when estimating your net proceeds to avoid surprises and to plan accordingly for your remaining funds.

How Do Prepayment Penalties Impact What You Earn from the Sale?

If your mortgage includes a prepayment penalty, it can reduce the proceeds from the sale. A prepayment penalty is a fee charged by the lender if you pay off your mortgage early, which is common when selling the property. Typically, these penalties range from up to 2% of your principal balance within the first two years, and 1% in year three. For example, if you owe $200,000 and are within the first year, the penalty could be as much as $4,000. This fee will be deducted from your proceeds at closing, reducing your net earnings. Understanding this potential cost helps you accurately plan your finances and avoid unexpected reductions in your earnings.

How are Prorated Taxes and Insurance Settled at Closing?

Prorated taxes and insurance on a mortgaged home are typically settled by the closing agent (either the title company or attorney), who adjusts the amounts based on the closing date, with the buyer and seller sharing the costs for the period of ownership. The closing agent calculates the prorated portion of property taxes and homeowner’s insurance for the seller’s time in the home. For example, if property taxes are due in December and you sell in June, the seller will pay the buyer for the months they owned the home. This process affects your net proceeds, ensuring both parties pay only for their time in the property.

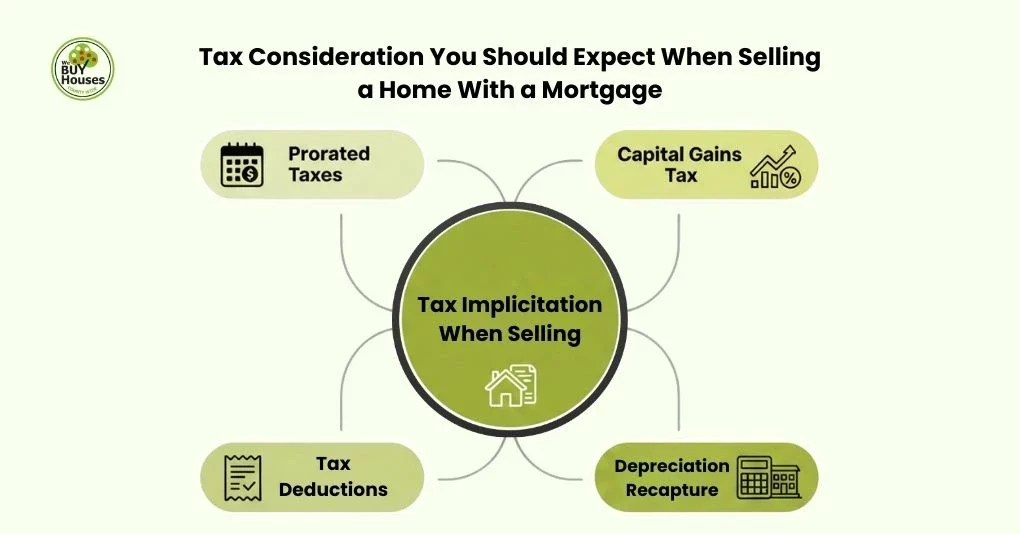

What Tax Considerations Should You Expect When Selling a Home With a Mortgage?

When selling a home with a mortgage, you may face capital gains tax on any profit from the sale, depending on your ownership and use of the property. If the home was used as a rental, you might also be subject to depreciation recapture taxes. Understanding these tax implications is essential to assessing how they will impact your final financial outcome.

How Do Capital Gains Taxes Apply When Selling Your Home With an Existing Mortgage?

Capital gains taxes apply if you sell your mortgaged home for more than your adjusted basis (purchase price plus improvements). The capital gain is calculated using the formula:

Capital Gain = Sale Price − Adjusted Basis − Selling Expenses

If the home was your primary residence for at least two of the last five years, you may qualify for a capital gains exclusion of up to $250,000 for single homeowners and $500,000 for married couples. Any profit beyond the exclusion may be taxed. Understanding these rules helps you determine the potential tax impact of your sale.

How Does Your Mortgage Payoff and Home Equity Affect Potential Taxable Gains?

Your mortgage payoff and home equity directly affect your taxable gains by determining how much profit you make from the sale of your home. Home equity is the difference between your home’s market value and the mortgage balance. If you have positive equity, the profit from the sale (after paying off the mortgage and closing costs) will be subject to capital gains tax if it exceeds the exclusion limits. However, if you are underwater (owing more than the home’s value), there may be no taxable gain, but you might need to cover the shortfall through a short sale.

What Tax Exclusions or Deductions Can You Qualify For When Selling a Home With a Mortgage?

When selling a home with a mortgage, you may qualify for several tax exclusions and deductions that can reduce your taxable gain, including:

- Capital Gains Exclusion: Up to $250,000 for singles and $500,000 for married couples filing jointly.

- Selling Expenses: Agent commissions, closing costs, marketing expenses, home staging costs, and repairs.

- Capital Improvements: Major upgrades like kitchen renovations, roof replacement, adding a new bathroom, or energy-efficient installations.

- Mortgage Interest: Interest paid on the mortgage up until the sale date.

- Property Taxes: State and local taxes (SALT), prorated for the year of the sale.

- Pre-sale Repairs: Costs of necessary repairs like fixing plumbing issues, painting, or replacing broken appliances.

- Homeowners Association (HOA) Fees: Prorated fees if applicable.

How Does Depreciation Recapture Apply When Selling a Mortgaged Home Used as a Rental or Investment Property?

When selling a mortgaged home used as a rental or investment property, depreciation recapture requires you to pay taxes on the depreciation deductions you have claimed during ownership. Depreciation recapture is the IRS policy requiring homeowners to pay the depreciation amount claimed back into their taxable income, taxed at up to 25% (Section 1250). For example, if you claimed $20,000 in depreciation, that amount will be taxed when you sell the property. Understanding this helps you accurately calculate your taxable gain and prepare for the potential tax liability.

How Are Prorated Property Taxes Handled at Closing When You Still Have a Mortgage?

When selling a home with a mortgage, prorated property taxes are calculated at closing to divide the tax responsibility between the seller and buyer based on the ownership period. The closing agent (either the title company or attorney) calculates the seller’s share of the property taxes, which is then deducted from the seller’s proceeds or credited to the buyer. For example, if property taxes are due in December and you sell in June, the seller will pay the buyer for the six months they owned the property. This ensures each party pays only for the time they owned the home.

What Happens When You Sell a House with Negative Equity?

When selling a house with negative equity, the sale proceeds will be insufficient to pay off the full mortgage balance, resulting in a shortfall. In this situation, you may need to bring out-of-pocket cash to cover the difference, or explore alternatives such as a short sale, where the lender agrees to accept less than the owed amount. Another option is a deed-in-lieu (DIL) of foreclosure, where you voluntarily transfer the property to the lender to avoid the foreclosure process. Understanding these options helps you navigate the sale and minimize financial strain.

Can You Sell Your Home If You Owe More Than It’s Worth?

Yes, you can sell your mortgaged home if you owe more than it’s worth, but the sale proceeds may not cover the full mortgage balance, creating a shortfall. You may need to bring out-of-pocket cash to pay the deficiency or negotiate a short sale, where the lender accepts less than the owed amount, or initiate a deed-in-lieu (DIL) of foreclosure. A DIL can help you avoid foreclosure, protecting your credit better than a foreclosure would. Understanding these options will help you manage the situation and minimize financial impact.

How Do Short Sales Work for Underwater Homeowners?

A short sale for underwater homeowners requires lender approval and proof of financial hardship to sell the property for less than the mortgage balance. The lender may forgive the remaining balance and accept a reduced payoff. A short sale also results in a smaller impact on your credit score (typically a 50-100 point drop) compared to foreclosure, which can drop it by 200-300 points. It also offers a quicker resolution, allowing you to move on sooner. Despite its challenges, a short sale is a viable option for homeowners with negative equity.

When Might You Need to Bring Cash to Closing?

You may need to bring cash to closing if the sale price of the mortgaged house does not cover the mortgage balance. This can happen if the home is underwater, there are high closing costs (fees for loan, appraisal, title), or there are outstanding liens (taxes, insurance). For example, if you owe $250,000 and the sale price is $230,000, you will need to cover the $20,000 difference.

What Are the Credit Implications of Selling at a Loss?

Selling a mortgaged house at a loss, such as through a short sale, which is reported as “settled for less than owned, can lower your credit score by 100-150 points, while a foreclosure typically causes a 200-300 point drop. Although a short sale has a less severe impact than foreclosure, both can make it harder to secure future loans or credit. Understanding these credit implications is crucial when deciding how to proceed with a home sale.

How Do Bridge Loans and Outstanding Mortgages Work When Buying and Selling?

A bridge loan helps homeowners buy a new home while still carrying an outstanding mortgage on their current property, using the equity in the current home as collateral. This temporary financing covers the down payment or other costs of the new home while the homeowner continues paying the existing mortgage until the current property is sold. The lender will assess the homeowner’s debt-to-income (DTI) ratio, which may be impacted by managing two mortgages. Understanding how a bridge loan works with an outstanding mortgage helps ensure homeowners can manage both financial obligations.

Bridge Loans for Buying and Selling

A bridge loan is a short-term loan that helps homeowners buy a new home before selling their current one, secured by the equity in the current property. It covers costs like the down payment while you continue paying the existing mortgage until the property is sold. The lender will evaluate the homeowner’s ability to manage both loans, considering the impact on their debt-to-income (DTI) ratio. While a bridge loan can simplify the transition between homes, it is important to understand higher interest rates, a short repayment period, and the challenge of managing two mortgages.

Outstanding Mortgage Obligations During the Buying-and-Selling

When buying a new home while still carrying an outstanding mortgage on your current property, you must continue making payments on the existing mortgage until the home is sold. The mortgage lender will assess your debt-to-income (DTI) ratio, which may be impacted by managing both loans at once. If there is a timing gap between the sale of your current home and the purchase of the new one, you could be responsible for paying two mortgages temporarily. Understanding how to balance these obligations is crucial to avoiding financial strain during the buying and selling process.

Debt-to-Income Risks With Two Mortgages

Carrying two mortgages can increase your debt-to-income (DTI) ratio, making it harder to qualify for a new mortgage or secure favorable terms. Maintaining both mortgages can also strain your cash flow, especially if your current home takes longer to sell, leading to higher default risks and a greater chance of falling behind on payments. The added financial burden can result in a strained monthly budget and increase the foreclosure risk if payments become unmanageable. To mitigate these risks, consider lowering your DTI, increasing your down payment, building cash reserves, and working with a lender who aligns with your financial goals.

Mortgage Timing Overlap

Mortgage timing overlap occurs when the closing dates for buying and selling do not align perfectly, leaving you responsible for two mortgages. This overlap can put pressure on your cash flow and increase your debt-to-income (DTI) ratio, making it harder to manage both mortgage payments. To minimize this risk, consider strategies like selling first and buying second, using a bridge loan to cover the new down payment, or arranging a concurrent closing. Additionally, tapping into a HELOC (Home Equity Line of Credit) can provide short-term financing to ease the transition.

How Do You Sell a House Under Delinquency, Default, or Forbearance?

To sell a house under delinquency, default, or forbearance, work with your lender to get approval and address any overdue payments. If the house is delinquent, you will need to bring the mortgage current, whereas in default, a Notice of Default (NOD) may require full repayment, often through a short sale. In forbearance, deferred payments must be paid when the home is sold. In all cases, lender approval is required, and sale proceeds may need to cover outstanding amounts. Exploring options like short sales or deed-in-lieu (DIL) can help avoid foreclosure.

How Do You Sell While Behind on Mortgage Payments (Delinquency Rules)?

To sell a home while behind on mortgage payments, you must contact the lender, get the payoff statement, assess the home’s value, list the property with a real estate agent or as FSBO, and close the deal to pay off the mortgage balance. The lender may require you to bring the mortgage current or accept a short sale if the sale price will not cover the full mortgage balance. Throughout this process, it is crucial to communicate with the lender to ensure their approval and avoid foreclosure.

How Do You Sell a House After Receiving a Notice of Default?

To sell a house after receiving a Notice of Default (NOD), contact the lender to obtain a payoff statement, explore loss mitigation options, hire a foreclosure-specialized agent, and prepare the house for sale. If the sale price does not cover the full mortgage amount, you may need to negotiate a short sale with the lender. Acting quickly is crucial, as the foreclosure process will continue if the sale is not completed in time, potentially leading to further financial and credit damage.

How Do You Sell a House During Mortgage Forbearance?

To sell a house during mortgage forbearance, notify your lender, assess the home’s equity, list the property, price strategically, and proceed with the sale. You must confirm with the lender whether any deferred payments or arrears need to be repaid at closing, as these amounts will need to be settled before the mortgage is considered fully paid off. If the sale proceeds do not cover the total owed, including the deferred payments, you may need to negotiate a short sale. Collaborating with the lender and understanding the specific terms of the forbearance agreement is essential to ensuring a smooth and successful sale process.

How Can You Avoid Foreclosure Through a Timely Sale?

To avoid foreclosure through a timely sale, act immediately and contact a HUD-approved counselor, prepare for a fast sale, and consider selling options like short sale or deed-in-lieu (DIL). Pricing the home competitively and being transparent about the situation helps attract serious buyers. If you are selling a house in foreclosure, it is important to move quickly before the lender takes full control of the property. By understanding your options and acting fast, you can prevent foreclosure and minimize its impact on your credit.

Can a Buyer Assume Your Mortgage?

Yes, a buyer can assume your mortgage if it is an assumable loan, such as those backed by FHA, VA, or USDA programs, but it requires lender approval. These types of loans typically allow buyers to take over your mortgage, provided they meet the lender’s qualification criteria. Most conventional loans, however, do not permit assumption unless specifically stated in the loan agreement. Even if the loan is assumable, you may remain liable for the debt unless the lender formally releases you from responsibility. It is important to verify with the lender whether an assumption is possible and understand the terms.

When Are FHA, VA, and USDA Mortgages Assumable?

FHA, VA, and USDA mortgages are assumable under specific conditions, such as meeting the lender’s creditworthiness requirements and adhering to government guidelines. For FHA loans, the buyer must meet standard FHA loan requirements, including a minimum down payment of 3.5% and a credit score of at least 580. VA loans can be assumed without military service, but the lender will evaluate the buyer’s credit, typically looking for a credit score of 620 or above. For USDA loans, the buyer must have a credit score of 620, meet income limits, and adhere to location requirements unless it is a family transfer, in which case the same terms may apply.

How Does Loan Assumption Affect Your Remaining Liability as the Seller?

When a buyer assumes your mortgage, you may remain secondarily liable unless the lender provides a full release (novation). This means that even though the buyer takes over the mortgage payments, you could still be responsible if the buyer defaults. A release of liability from the lender is essential to fully remove your responsibility. If the lender does not grant this release, you may be at risk of being held accountable for the loan in case of default. Understanding the terms and negotiating with the lender is crucial to ensure that you are no longer financially tied to the mortgage after the assumption.

How Can You Buy and Sell at the Same Time When You Still Have a Mortgage?

To buy and sell a home at the same time while still having a mortgage, you can use strategies like bridge loans, selling first and buying second, or concurrent closings. A bridge loan provides short-term financing to cover the down payment while your current home is still on the market. Selling first and using the proceeds for your next purchase is another option. Alternatively, concurrent closings allow both transactions to happen on the same day, minimizing the risk of carrying two mortgages.

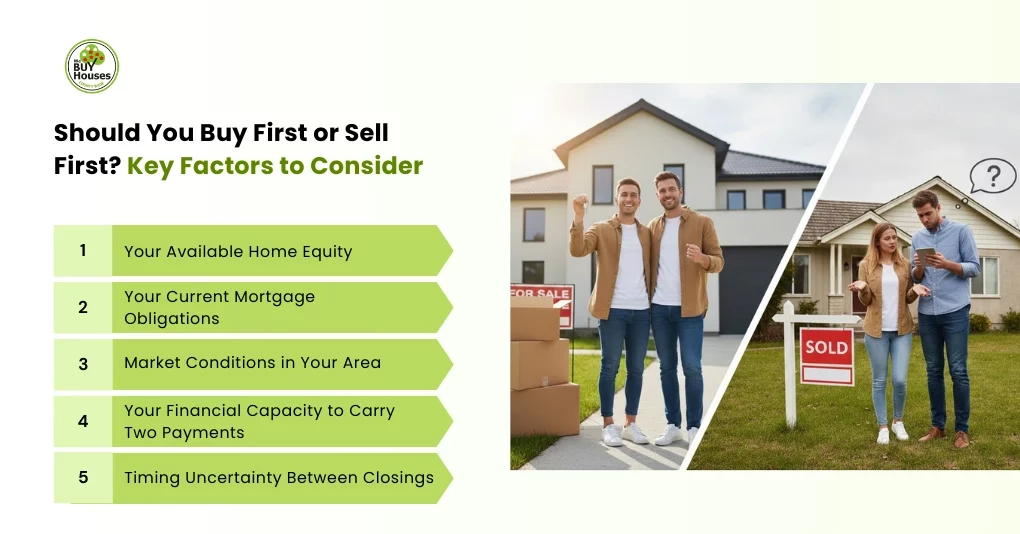

Should You Buy First or Sell First? Key Factors to Consider

Deciding whether to buy first or sell first depends on your available home equity, current mortgage obligations, market conditions, financial capacity to carry two payments, and timing uncertainty between closings. Buying first can strain your finances if you manage two mortgages, while selling first provides cash for a down payment but may leave you without a home temporarily. Evaluating these factors will help you determine the best strategy for your situation and the current real estate environment.

5 factors influencing homeowners’ decision to buy or sell first are:

- Your Available Home Equity

If you have significant equity, you can use the proceeds from your home sale as a down payment for your next home, reducing the need for additional financing. Limited equity may require you to seek alternative solutions, like a bridge loan, to bridge the gap between the sale and purchase.

- Your Current Mortgage Obligations

If you still have a substantial balance left on your current mortgage, managing two mortgage payments can strain your budget. By selling first, you can use the sale proceeds to pay off the current mortgage, easing the financial burden of securing a new loan.

- Market Conditions in Your Area

In a seller’s market, where demand is high, selling first can help you capitalize on the higher sale price. However, in a buyer’s market, where inventory is abundant, buying first may give you more time to find the right property at the best price.

- Your Financial Capacity to Carry Two Payments

If you have sufficient cash reserves and a strong debt-to-income ratio, you might be able to manage two mortgages temporarily. However, if you are financially stretched, selling first provides relief by eliminating one mortgage obligation and reducing financial strain.

- Timing Uncertainty Between Closings

If the closing dates do not align, you may have to carry two properties, which can create financial stress. To avoid this, selling first allows you to use the proceeds for your next home purchase. If buying first is necessary, consider using a bridge loan or finding temporary housing to cover any gaps until your old home sells.

How Your Existing Mortgage Affects Your Purchasing Power?

Your existing mortgage affects your purchasing power by impacting your debt-to-income (DTI) ratio, which lenders use to determine how much you can borrow for a new home. The higher your current mortgage payments, the less you can afford on a new loan. For example, if your current mortgage payment is $2,000 per month and you earn $6,000 per month, your DTI ratio is 33%. According to the 1/10 rule, if interest rates increase by 1%, you may lose up to 10% of your purchasing power. If you were previously able to afford a home priced at $300,000, a 1% rate hike could reduce your buying power to $270,000. Reducing your current mortgage payments or selling your home first can increase your ability to afford a higher-priced property.

How Do You Manage Two Mortgages Temporarily?

To manage two mortgages temporarily, you can use methods such as bridge loans, renting out your current property, or using cash reserves to cover both payments. A bridge loan can provide short-term financing to help with the down payment on your new home while you wait for your current home to sell. Renting out your current home can generate income to cover mortgage payments, and cash reserves can provide a buffer until your home sells. It is important to evaluate your financial capacity and plan carefully to avoid overwhelming your budget during this period.

How Can You Use Sale Proceeds for Your Next Home’s Down Payment?

You can use the proceeds from the sale of your current home for the down payment on your next home by selling the property and applying the funds toward the purchase via a bridge loan or HELOC. After covering closing costs and paying off your mortgage, the remaining sale proceeds can be used as your down payment. This reduces the amount you need to borrow, improving your loan terms. Selling first gives you the flexibility to use the full amount as a down payment, ensuring a smoother transition to your new home.

What Legal and Lender Requirements Should Sellers Be Aware Of?

Sellers should be aware of legal and lender requirements, including clearing the title, satisfying liens, and obtaining a payoff statement from the lender. The title company ensures the title is clear and any outstanding liens, such as home equity lines of credit (HELOC) or mechanic’s liens, are settled before ownership transfers. Sellers must also ensure their mortgage obligations are paid off, with lender approval of the final payoff amount. Understanding the required documentation and the lender’s role is key to ensuring a smooth sale process.

How Are Lien Releases, HELOC Payoffs, and Second Mortgages Handled?

When selling a home with multiple liens, lien releases, HELOC payoffs, and second mortgages must be paid off before the property can transfer to the buyer. The title company will coordinate with the lenders, requesting payoff statements for each lien, and ensure the outstanding balances are paid. Once the debts are settled, the lenders will issue a lien release, clearing the property’s title for the transfer. If the sale proceeds do not cover the full payoff amount, you may need to negotiate a short sale or contribute additional funds to clear the liens. Ensuring all liens are resolved is crucial for a smooth closing.

What Happens If Your Loan Has an Acceleration Clause?

If your loan has an acceleration clause, the lender can demand the full balance of the mortgage if certain conditions are met, such as missed payments or violating loan terms. This means the lender can accelerate the loan, requiring immediate repayment of the remaining mortgage balance, even if you are not behind on payments. If you sell the property, you may be required to pay off the entire remaining mortgage balance upfront, which could complicate the sale if the proceeds are insufficient.

What Documents Are Required for Lender Payoff and Closing Clearance?

To clear the lender payoff and finalize the closing on a house with a mortgage, you need a payoff statement from the lender, a lien release, and the closing disclosure. You will also need a photo ID, homeowners’ insurance proof, promissory note, and deed of trust. In addition, the initial escrow statement, Certificate of No Objection (NOC) (if applicable), and updated title insurance policy will be required. Additionally, documents related to any outstanding liens, such as HELOC or second mortgage payoffs, may be required. The title company will ensure all necessary documents are in place for a smooth closing and confirm the mortgage is fully paid off before the property transfers.

How Do Title Companies Ensure a Clear Transfer of Ownership?

Title companies ensure a clear transfer of ownership by conducting a thorough title search to verify the property’s legal ownership and identify any outstanding liens or claims. They check for issues like unpaid taxes or mechanics’ liens that could affect the sale. Once the title is clear, the company provides title insurance to protect the buyer and lender. The title company also coordinates lien releases, ensuring mortgages or liens are paid off, and records the deed at closing to complete the transfer of ownership.

What Alternatives Do You Have If Your Mortgage Balance Makes Selling Difficult?

If your mortgage balance makes selling difficult, you can consider renting the house, refinancing the house, selling the home to a cash buyer, or selling the home as-is. Renting covers mortgage payments, refinancing lowers monthly costs, and selling as-is or to a cash buyer offers quick sales, though often at a lower price. These options help if your mortgage exceeds the home’s value.

Should You Rent Out Your Home Instead of Selling?

Renting out your home instead of selling can be a viable option if you are not ready to sell or if the market conditions are not favorable. It allows you to maintain ownership and generate rental income to cover your mortgage. For example, if your mortgage is $1,500 and you rent for $2,000, the income offsets your costs. However, being a landlord involves maintenance, tenant management, and long-term expenses like property taxes, insurance, and market trends. Renting could be a good strategy if you anticipate home value appreciation or want to keep the property for future sale when conditions improve.

Should You Refinance Before Selling?

Refinancing your house before selling may be a good option if you need to reduce monthly payments or unlock equity for another investment. However, if you plan to sell soon, refinancing may not recoup its costs, such as closing fees and appraisals. If you are staying longer than expected, refinancing could lower your mortgage rate and improve financial flexibility. Consider your timeline, refinancing costs, and future plans to determine if it is worthwhile.

Should You Sell to a Cash Buyer for Speed and Convenience?

You should sell your mortgaged house to a cash buyer for speed and convenience if you are relocating, want to avoid foreclosure, or if your house needs major repairs and renovations. Cash buyers can expedite the process by bypassing financing approvals and appraisals, leading to a faster closing. However, cash offers are often lower than those from buyers using traditional financing. If your priority is a quick, hassle-free sale, selling to a cash buyer may be a suitable choice, but be sure to weigh it against your financial goals and needs.

When Does Selling the Home As-Is Make Financial Sense?

Selling the home as-is makes financial sense if your property needs significant repairs, you lack the funds for renovations, or you want to avoid the hassle of preparing the house for sale. This option allows you to save on repair costs, time, and effort while selling quickly, especially in a competitive market. However, selling the house as-is may lead to lower offers, as buyers will account for the cost of repairs. If your primary goal is a fast sale and avoiding upfront expenses, selling as-is could be the right choice for your situation.

Frequently Asked Questions About Selling a House With a Mortgage

When Do You Stop Paying Your Mortgage During the Sale?

You stop paying your mortgage once the home sale is finalized and the transaction closes. The lender will receive the sale proceeds through escrow, and any remaining mortgage balance will be paid off at that time. After the sale, you are no longer liable for mortgage payments on the property, as the loan is considered paid off.

Does Selling a House Affect Your Credit Score?

Selling a home does not directly impact your credit score. However, if the sale pays off your mortgage, it can improve your credit by reducing your debt-to-income ratio. If the mortgage is not paid off or you default, it could negatively affect your credit due to missed payments or foreclosure.

Can You Sell Soon After Refinancing Your Mortgage?

Yes, you can sell soon after refinancing, but be aware that many lenders charge a prepayment penalty if you sell within the first few years. Additionally, refinancing may reset your loan terms, so selling too soon could prevent you from fully benefiting from a better interest rate.

What Happens to Escrow Funds After You Sell Your Home?

After the sale, the escrow company pays off your mortgage, agent commissions, taxes, and other fees, and your mortgage lender will refund any remaining money in your escrow account within 20 business days. If proceeds exceed your mortgage balance, you will receive the surplus. In case of negative equity, you may owe the difference.

Can You Transfer Your Mortgage to Another Home?

Most mortgages are not transferable to a new home because the loan is tied to the specific collateral. As a result, you will need to pay off the current mortgage and apply for a new one when purchasing a new property. In some cases, a “portable mortgage” may allow a transfer, but this option is rare and often comes with specific conditions and fees.

How Soon After Buying Can You Sell Without Penalty?

You can sell your home anytime after buying, but doing so soon could lead to financial penalties or tax implications. If sold within the first few years, you may face capital gains tax unless the property was your primary residence for at least two of the last five years. Additionally, some mortgages have prepayment penalties. It is best to consult a tax professional to assess potential costs.