Many Bay Area seniors find themselves “house-rich but cash-poor.” According to AARP, more than 70% of older homeowners have the majority of their wealth locked in their property, while their monthly income often depends solely on Social Security or a modest pension. This situation creates an equity trap where seniors own valuable homes but face limited financial flexibility to manage living costs, medical expenses, or unexpected needs. The burden of high property taxes, ongoing maintenance, and rising care expenses only deepens this imbalance, leaving retirees with significant assets but little day-to-day stability.

One solution is to convert home equity into a source of steady income. Seniors in San Francisco and Walnut Creek can sell their properties in as-is condition, avoiding the delays and costs of traditional real estate listings. By reinvesting the proceeds into retirement-focused funds such as Vanguard’s S&P 500 ETF (VOO) or the Target Retirement Income Fund (VTINX), they can transform illiquid assets into a predictable cash flow. This shift offers more than just financial relief; it creates freedom of choice in retirement, enabling seniors to cover essential costs with confidence and enjoy greater flexibility in how they live their later years.

What Are the Equity Traps Faced by Senior Homeowners?

Senior homeowners in the Bay Area face several equity traps: locked wealth, fixed income limits, mortgage debt, and rising care costs. Each challenge reduces the ability to turn property value into practical retirement income.

Locked wealth arises when most retirement savings sit in a home that cannot easily be converted into cash. Selling often takes months, while borrowing against equity involves high interest or strict qualifications. Fixed income limits occur when Social Security and small pensions fail to keep pace with rising property taxes, insurance, and upkeep. In 2025, the average Social Security benefit is $1,976 per month, and even with a modest $1,000 pension, many retirees fall short of covering Bay Area costs. Mortgage debt creates further stress. Seniors with outstanding balances risk falling behind on payments, which can trigger foreclosure or forced sales. Finally, care costs add heavy pressure. Assisted living typically ranges from $3,500 to $4,000 per month, far beyond what a fixed income can support.

AARP estimates that over 10 million seniors are house-rich but cash-poor, often holding more than $500,000 in equity that remains locked away while daily financial needs go unmet. These equity traps highlight the gap between property value and retirement security. A home may look like a strong asset on paper, yet without liquidity, it becomes a burden that limits choices, creates stress, and restricts independence. Recognizing these traps is the first step toward converting housing wealth into reliable, usable income.

How Can Seniors Sell Their Homes Quickly and As-Is?

Selling a home in retirement does not have to mean repairs, staging, or long delays. Seniors in San Francisco and Walnut Creek can work with cash home buyers like We Buy Houses County Wide, who specialize in as-is sales, offering a fast and straightforward process.

- Step 1: Request an Assessment

Buyers evaluate the home’s condition, regardless of repairs needed. No inspections or upgrades are required.

- Step 2: Receive a Cash Offer

Within 24 hours, a fair offer is presented based on the current market value. Seniors can review the terms with family or advisors before accepting.

- Step 3: Close Within 7–14 Days

Escrow moves quickly, often finishing in two weeks. No realtor commissions or hidden fees reduce the net amount received.

- Step 4: Clear Existing Mortgages

Any outstanding loan balance is paid directly from the sale proceeds, leaving the seller debt-free.

Real examples highlight the difference:

- A Walnut Creek senior sold a condo in its original 1970s condition, closed in 10 days, and walked away with $400,000 in net proceeds.

- A San Francisco retiree accepted an all-cash offer that cleared a $120,000 mortgage and left $350,000 available for reinvestment.

Quick as-is sales protect dignity, save time, and provide seniors with immediate access to housing wealth that can be reinvested into reliable retirement income.

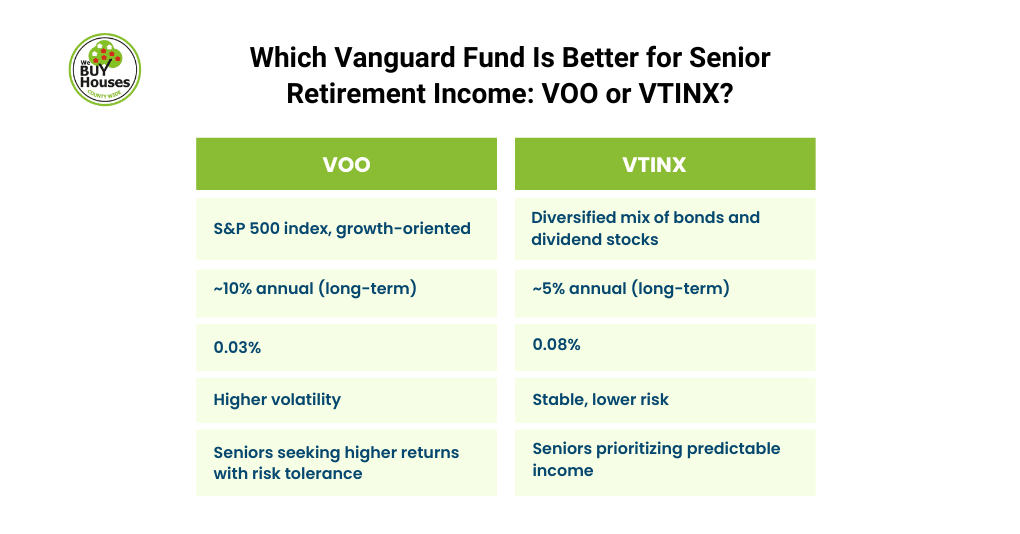

Which Vanguard Fund Is Better for Senior Retirement Income: VOO or VTINX?

Two Vanguard options stand out for seniors converting home sale proceeds into retirement income: the Vanguard S&P 500 ETF (VOO) and the Vanguard Target Retirement Income Fund (VTINX). Each serves a different purpose, and the right choice depends on whether a retiree values steady income or long-term growth potential.

| Fund | Focus | Average Return* | Expense Ratio | Risk Profile | Best For |

| VOO | S&P 500 index, growth-oriented | ~10% annual (long-term) | 0.03% | Higher volatility | Seniors seeking higher returns with risk tolerance |

| VTINX | Diversified mix of bonds and dividend stocks | ~5% annual (long-term) | 0.08% | Stable, lower risk | Seniors prioritizing predictable income |

*Based on historical averages. Past performance does not guarantee future results.

How Much Income Can You Earn Monthly After Selling Your Home?

Reinvesting $400,000 into VOO could yield around $40,000 annually, or about $3,300 per month, though income varies with market swings. The same amount in VTINX might generate closer to $17,000 annually, or $1,400 per month, with less volatility.

Morningstar consistently rates both funds highly, but their roles differ. VOO favors growth-oriented retirees who can manage short-term fluctuations, while VTINX prioritizes income stability and reduced exposure to downturns. Seniors unsure which approach suits them should consult a fiduciary advisor to align fund choice with risk tolerance, health outlook, and lifestyle needs.

By weighing these trade-offs, retirees can choose a strategy that not only fits financial goals but also provides confidence and flexibility in retirement.

What Tax Implications Should Seniors Consider?

Projected income must be reviewed alongside tax obligations. Dividends from VOO and VTINX are generally taxable, and withdrawals may be subject to income tax depending on whether the funds are held in taxable accounts or retirement accounts like IRAs. The IRS also requires retirees over age 73 to take Required Minimum Distributions (RMDs) from traditional retirement accounts, which can impact cash flow planning.

For homeowners selling a longtime residence, the IRS capital gains exclusion offers significant relief: up to $250,000 for individuals or $500,000 for married couples if residency and ownership conditions are met. Considering these rules ensures that seniors evaluate not just gross returns but also the after-tax income available to support retirement needs.

What Do Real Senior Home Sellers in the Bay Area Experience?

Senior homeowners who choose to sell often see dramatic improvements in both income and lifestyle. Two local cases illustrate how selling a long-held property and reinvesting proceeds can transform retirement security.

A Widow’s Journey: Sunset District to Senior Living

San Francisco: A 78-year-old widow in the Sunset District sold her fixer-upper for $450,000 in just 9 days. She reinvested her proceeds into the Vanguard Target Retirement Income Fund (VTINX), generating roughly $15,000 per year in dividends. That steady stream lifted her income from $2,500 per month to $4,500 per month. With the additional funds, she moved comfortably into a senior living community and gained the stability to cover care costs without financial stress.

Rossmoor Veteran Turns Cluttered Condo into Travel Fund

Walnut Creek: An 80-year-old veteran living in Rossmoor sold his cluttered condo for $400,000. Choosing the Vanguard S&P 500 ETF (VOO), he secured an expected return of about $40,000 annually. His monthly income rose from $3,000 to $6,333, giving him the freedom to travel, visit grandchildren, and support a more active retirement.

Why Might 2025 Be the Right Time for Seniors to Sell Their Homes?

According to Zillow’s Bay Area housing market forecast, average home values in San Francisco–Oakland–Hayward are expected to fall by about 6.1% by June 2026. RealtorZee’s 2025 outlook adds that prices could decline 1.7% by October 2025 as higher mortgage rates and slower job growth weigh on demand. For seniors who depend on home equity for retirement, delaying a sale risks losing tens of thousands of dollars in value if these predictions hold true.

On the investment side, Morningstar reported in January 2025 that Vanguard announced its largest fee cut to date, lowering expense ratios on nearly 90 funds. The change is expected to save investors more than $350 million collectively in 2025, making retirement-focused funds like VOO and VTINX even more cost-efficient.

Together, these market signals point to a clear conclusion: 2025 offers seniors a strategic window to protect accumulated equity and reinvest under favorable conditions. Acting now means securing today’s home values while benefiting from reduced investment costs, creating a more stable foundation for monthly retirement income.

Ready to turn your home equity into reliable retirement income?

Call 925-587-9740 or get an offer to learn how you can sell quickly, reinvest with confidence, and reclaim financial freedom. Share this with a senior you care about and help them thrive in their golden years.