Yes, you can sell a house in foreclosure, as it helps avoid the long-term consequences of foreclosure, such as damage to your credit. If the property is still in pre-foreclosure, you have more flexibility to sell through a traditional sale or short sale with the lender’s approval. Even after foreclosure proceedings have begun, you can still sell the property, but it requires coordinating with the lender to close before the auction.

The steps to sell a house in foreclosure involve verifying your foreclosure status, contacting your lender, and choosing the best selling strategy based on your situation. If you are underwater on the mortgage, a short sale may be necessary, while pricing the home competitively and marketing it quickly are crucial to avoid an auction. Working with real estate agents or cash buyers can speed up the process.

If you can’t sell in time, alternatives like a deed in lieu, loan modification, or bankruptcy protection can help you avoid foreclosure. Understanding your state’s foreclosure laws (judicial or non-judicial foreclosure) and timelines is essential for making the right decision. Consulting with a foreclosure attorney or a HUD-approved housing counselor ensures you are aware of all your options.

What Does It Mean When a House Is in Foreclosure?

A house in foreclosure means the homeowner has missed required mortgage payments, and the lender or lien holder has started the legal process to sell the property to recover the unpaid loan. This happens after a mortgage loan enters default, the lender enforces its mortgage lien, and official action, such as a Notice of Default (NOD) or a court filing, is recorded under state foreclosure laws. When a house goes into foreclosure, it is placed on a defined foreclosure timeline that begins after several months of delinquency, most often 90 to 120 days. The foreclosure process then moves forward through judicial or non-judicial procedures and can lead to a foreclosure auction if the default is not resolved through payment, lender-approved relief, or a home sale within the allowed time.

What Happens When Your House Goes Into Foreclosure?

When your house goes into foreclosure, the lender begins legal action to recover the unpaid mortgage, putting the home at risk of being sold to recoup their losses. The homeowner receives formal notices, such as a Notice of Default or court or trustee filings, and the loan may be accelerated as arrears and fees increase. If the default is not resolved within the allowed time, the foreclosure process can move through judicial or non-judicial procedures, leading to a foreclosure sale, possible eviction, and significant damage to the homeowner’s credit score.

When Does a House Go Into Foreclosure?

A house goes into foreclosure after a homeowner misses mortgage payments long enough for the loan to enter default, usually 90 to 120 days. At that point, the lender enforces the mortgage lien and issues required notices, such as a Notice of Default or a court filing, under state foreclosure laws. Federal servicing rules generally prevent lenders from starting foreclosure proceedings until a loan is at least 120 days delinquent, although exact timing varies by state and by whether the process is judicial or non-judicial.

Why Do Houses Go Into Foreclosure?

Houses go into foreclosure because homeowners can no longer make mortgage payments, and the loan remains in default. Common causes include financial hardship, such as job loss, reduced income, medical expenses, divorce, or rising housing costs that make the mortgage unaffordable. In some cases, adjustable-rate mortgages reset to higher payments, or homeowners carry excessive debt from second mortgages, property tax liens, or HOA dues arrears. When these hardships persist, and the homeowner cannot reinstate the loan, obtain lender-approved relief, or sell the property, the lender proceeds with foreclosure to recover the unpaid balance.

How Does a House Go Into Foreclosure?

A house goes into foreclosure when the homeowner fails to resolve the default, and the lender begins legal action to recover the unpaid mortgage. This typically happens after 90 to 120 days of missed payments, triggering a Notice of Default. Depending on state laws, the foreclosure process can be judicial (requiring court involvement) or non-judicial (handled by a trustee). If the homeowner cannot resolve the default or sell the property, the lender can proceed with foreclosure, which may result in a home sale at auction.

How Long Before Your House Goes Into Foreclosure?

Your house goes into foreclosure after 90 to 120 days (four missed mortgage payments), depending on the lender and state laws. This period is considered pre-foreclosure, during which the lender may issue a Notice of Default that marks the formal start of the foreclosure process. In judicial states, the process can take longer because it requires court approval, while in non-judicial states, foreclosure may proceed faster. On average, the foreclosure process can take several months, but homeowners still have time to resolve the issue through options like loan modification or short sale before the property is sold at auction.

What Are the Steps to Sell a House in Foreclosure?

Selling a house in foreclosure involves determining the foreclosure status, contacting your lender for approval, evaluating your equity, pricing the home competitively, and selling the property before the foreclosure auction. Following this structured approach allows the homeowners to avoid the home being sold at auction, minimize damage to their credit, and potentially preserve some equity by completing the sale on their terms. It also provides homeowners with an opportunity to negotiate with the lender for a short sale or other alternatives that may offer more favorable outcomes.

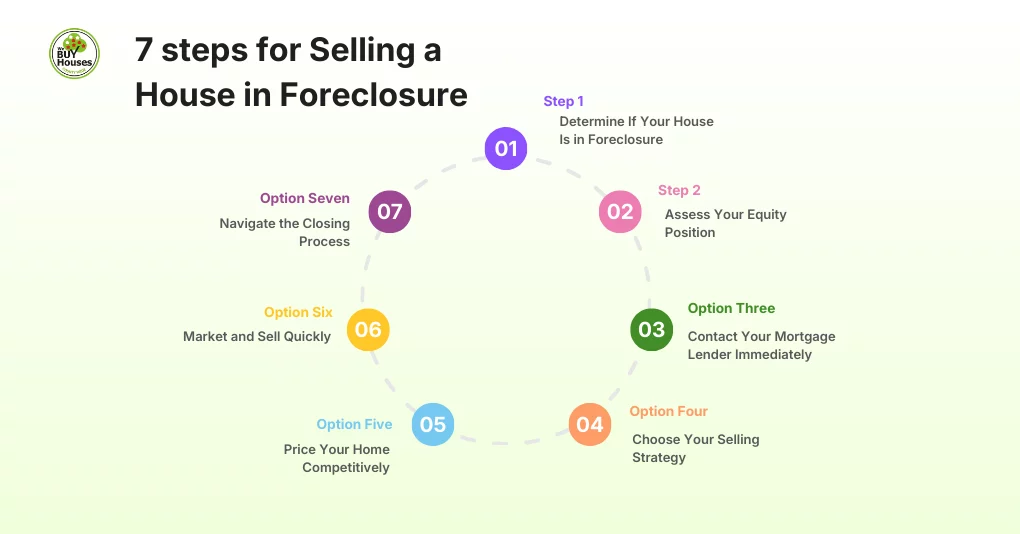

7 steps for selling a house in foreclosure are:

Step 1: Determine If Your House Is in Foreclosure

The first step in selling a house in foreclosure is to determine the foreclosure status by reviewing your mortgage statements, contacting your lender, or checking public records for a filed Notice of Default. You may also receive notices such as a Notice of Trustee Sale in non-judicial states or a court filing in judicial states. Understanding whether your home is in a pre-foreclosure or active foreclosure process will help you determine the next steps and how much time you have before the foreclosure auction.

Step 2: Assess Your Equity Position

The next step in selling a house in foreclosure is to assess your equity position, which is the difference between your home’s current market value and the remaining mortgage balance. To assess this, you can obtain a Comparative Market Analysis (CMA) from a real estate agent or an appraisal to determine your home’s fair market value (FMV). If you have positive equity (the home is worth more than what you owe), you may be able to sell it through a traditional sale, while if you are underwater (owe more than the home is worth), you may need to consider a short sale, where the lender accepts less than the full mortgage balance.

Step 3: Contact Your Mortgage Lender Immediately

After assessing your equity position, contact the mortgage lender to inform them of your intention to sell and discuss your available options. If you are considering a short sale, the lender must approve the sale price and terms. When contacting your lender, request a payoff statement to determine the total amount required to settle the mortgage and prevent foreclosure. Be prepared to provide necessary documentation, such as a hardship letter or financial statement, to support your case for a sale or alternative solutions, including a loan modification or forbearance.

Step 4: Choose Your Selling Strategy

Once you have contacted your lender, choose the best selling strategy to maximize your financial outcome and avoid foreclosure. The right approach will depend on your home’s equity, the timeline you are working with, and your lender’s willingness to cooperate. Choosing the most suitable option can help you avoid further complications and ensure the best possible outcome in a time-sensitive situation.

3 best-selling strategies for a foreclosure house are:

Option 1: Traditional Real Estate Sale

A traditional real estate sale involves listing your home with a real estate agent at market value. This option is ideal if you have positive equity and enough time to complete the sale before foreclosure proceedings move forward. It typically provides the highest sale price but requires preparation, buyer contingencies, and a longer timeline. Before proceeding, consider whether to sell by owner or use a realtor to determine which approach best fits your foreclosure timeline.

Option 2: Fast Cash Sale to Investors

A fast cash sale to investors offers a quick, straightforward solution, allowing you to sell the property in as-is condition without repairs or lengthy negotiations. Selling your house to an investor offers a quick, efficient way to avoid foreclosure and eliminate the risk of an auction. Though the sale price is typically lower than market value, this option allows for a fast closing, providing a streamlined way to move forward without the delays or uncertainty of traditional selling methods.

Option 3: Short Sale

A short sale occurs when your lender agrees to sell the property for less than the amount owed on the mortgage. This option is suitable if you are underwater and unable to sell for the full loan balance. While it can take time to get lender approval, it allows you to avoid foreclosure and its negative consequences, such as eviction and significant credit damage. Understanding how much you might lose when selling as-is can help you decide whether to pursue repairs or sell in the current condition.

Step 5: Price Your Home Competitively

Pricing your home correctly in a foreclosure situation is critical to avoid an auction and ensure a quick sale. A competitive price will help attract buyers swiftly, meeting the lender’s payoff requirements and reducing the risk of the property being taken back. A Comparative Market Analysis (CMA) can help set a price based on local market conditions, your home’s condition, and the amount owed on the mortgage. Pricing it too high can result in delays, while pricing it too low may not cover your loan balance, so finding the right balance is key.

Step 6: Market and Sell Quickly

To avoid foreclosure and maximize your chances of a successful sale, it’s crucial to market your home aggressively and efficiently. To attract serious buyers, list your property on multiple platforms, including MLS, Zillow, Realtor, and other real estate websites. Work with a real estate agent who has experience with distressed property sales and can help highlight the home’s best features, even in its current condition. Consider targeting cash buyers or real estate investors, as they may be more willing to move quickly and purchase the home as-is, further speeding up the process and potentially preventing foreclosure.

Step 7: Navigate the Closing Process

To finalize the sale and avoid foreclosure, it is crucial to navigate the closing process quickly and efficiently. Ensure that your lender receives the necessary payoff amount and documents to facilitate a smooth transaction. If you are pursuing a short sale, the lender must approve the offer before closing, which may take additional time. Work closely with your real estate agent, title company, and lender to resolve any liens or title issues, ensuring the sale closes before the foreclosure auction. This will help you avoid eviction and minimize damage to your credit. Also, be prepared for closing costs for sellers, which typically range from 1-3% of the sale price.

Alternative Options: What If You Can’t Sell in Time?

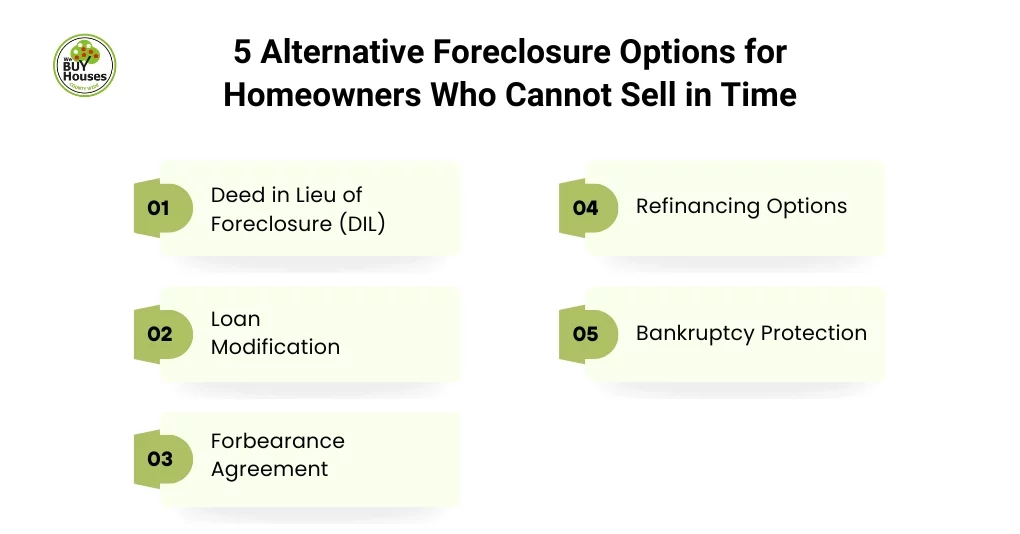

If you can’t sell your home in time to avoid foreclosure, options like a deed in lieu of foreclosure, loan modification, forbearance agreement, or bankruptcy protection can help you delay or prevent the foreclosure process. A deed in lieu lets you transfer the property to the lender, while a loan modification adjusts your mortgage terms. Forbearance agreements can pause or reduce payments, and bankruptcy may delay foreclosure. It is important to consult with a foreclosure attorney or a HUD-approved housing counselor to explore the best solution for your situation.

5 alternative foreclosure options for homeowners who cannot sell in time are:

Deed in Lieu of Foreclosure (DIL)

A deed in lieu of foreclosure is when a homeowner voluntarily transfers the property back to the lender for the cancellation of the mortgage debt. This option can help avoid the foreclosure process and minimize the damage to your credit, though it still has a negative impact, typically less than a full foreclosure. To qualify for a DIL, the property must be free of other liens, and you must prove financial hardship. While the lender may forgive the remaining debt, this is not guaranteed, and the lender may still pursue a deficiency judgment for any unpaid balance.

Loan Modification

A loan modification is a long-term solution for foreclosure where the lender adjusts your mortgage terms by lowering the interest rate, extending the loan term, or re-amortizing the balance. To apply, you must submit a hardship letter, income verification, and a loan modification request. Programs like FHA-HAMP or Flex Mod are common, but eligibility varies. The process typically takes 30–90 days and may include a trial period before permanent changes. If approved, foreclosure proceedings are paused, but if denied, the foreclosure timeline may resume. Be sure to follow up with your lender and consult CFPB or HUD-certified counselors to ensure eligibility and increase your chances of approval.

Forbearance Agreement

A forbearance agreement is a temporary arrangement with your lender that allows you to pause or reduce mortgage payments for a specified period, typically due to financial hardship. This includes job loss, medical emergencies, or a sudden drop in income. During the forbearance period, you may be able to temporarily reduce or skip payments, with the understanding that the missed payments will be repaid later. It is important to review CFPB forbearance protections and explore options available through FHA or VA loan programs for additional guidance. Be sure to understand the forbearance terms to avoid further foreclosure risk.

Refinancing Options

Refinancing allows you to replace your existing mortgage with a new one, potentially lowering your monthly payment, fixing an adjustable-rate mortgage (ARM), or extending the loan term. This can make your mortgage more manageable and help avoid foreclosure. Options like FHA Streamline Refinancing, VA IRRRL, or conventional refinancing are available for eligible homeowners, especially those at risk of foreclosure. However, refinancing may not be an option if you are behind on payments or have little equity. It is essential to discuss your situation with your lender to determine if refinancing is a viable solution.

Bankruptcy Protection

Bankruptcy protection can temporarily stop foreclosure proceedings by triggering an automatic stay, which halts all creditor actions, including foreclosure. This option provides time to reorganize finances, catch up on payments, or negotiate with the lender. Chapter 13 bankruptcy allows you to create a repayment plan over 3 to 5 years, while Chapter 7 can eliminate unsecured debts but may not stop foreclosure unless payments are brought up to date. To qualify for Chapter 13, you must have no prior bankruptcy petition dismissal within the last 180 days and a combined debt of less than $2.75 million. Bankruptcy has long-term credit effects, so it is essential to consult with a bankruptcy attorney to evaluate if this option is right for you.

What to Do If Your House Is in Foreclosure?

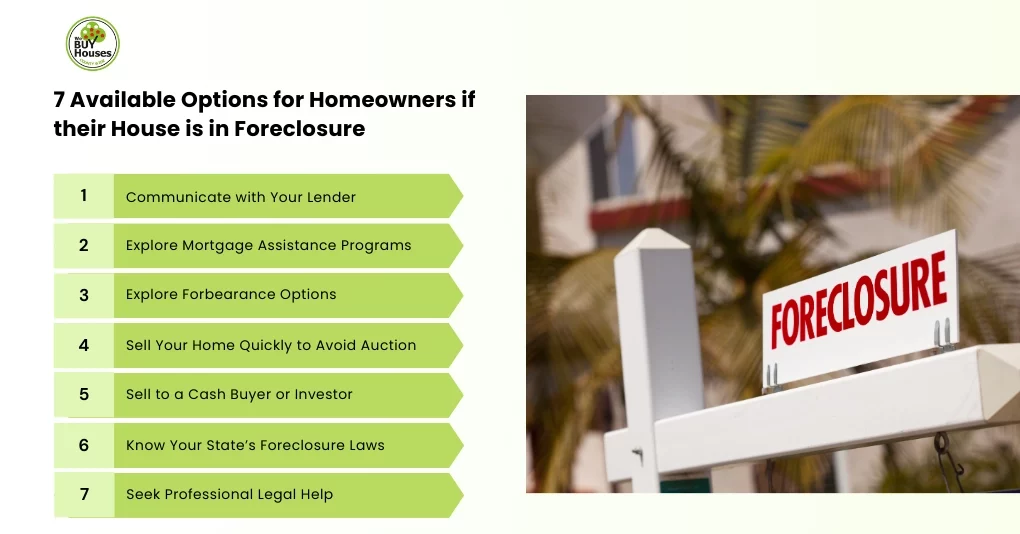

If your house is in foreclosure, immediately communicate with your lender to explore options like mortgage assistance programs, forbearance, a loan modification, or selling your home quickly to avoid auction. You may also consider selling to a cash buyer or real estate investor for a fast sale. Make sure you know your state’s foreclosure laws, as they can impact your rights and options. Additionally, seek professional legal help from a foreclosure attorney or a HUD-approved housing counselor to understand your options and protect your rights during the process.

7 available options for homeowners if their house is in foreclosure are:

Communicate with Your Lender

Contacting your lender early is crucial to exploring options like loan modification, forbearance, or a repayment plan to avoid foreclosure. Lenders often offer temporary relief for homeowners facing hardships such as job loss, medical issues, or divorce. Be prepared to explain your situation and provide documentation like proof of income and a hardship letter. Ask about all options, including short sale approval if needed. Take notes, request written confirmation of promises made, and follow up in writing. Timely communication is essential, as CFPB regulations require servicers to evaluate relief options if contacted within 120 days of delinquency.

Explore Mortgage Assistance Programs

Mortgage assistance programs are initiatives offered by the government, lenders, or nonprofit organizations to help homeowners struggling with mortgage payments and facing foreclosure. Programs like the Home Affordable Modification Program (HAMP), Homeowner Assistance Fund (HAF), or state-specific relief such as the California Mortgage Relief Program can reduce payments, extend loan terms, or provide temporary relief. To apply, you will need to provide income verification and a hardship letter. Eligibility varies, so research available programs and consult with a HUD-approved housing counselor to find the best solution for your situation.

Explore Forbearance Options

Forbearance allows homeowners to temporarily pause or reduce mortgage paymentsif they are facing financial hardship, such as job loss or medical emergencies. During this period, your lender may suspend payments or accept reduced amounts. Afterward, the missed payments will typically be due later, either as a lump sum or through a repayment plan. Programs like FHA, VA, and Fannie Mae/Freddie Mac offer specific forbearance options. It is important to discuss the terms with your lender to understand how the forbearance will work and what repayment options are available.

Sell Your Home Quickly to Avoid Auction

If you are facing foreclosure, selling your home quickly can be an effective way to avoid a foreclosure auction and reduce credit damage. By selling your house before the auction date, you can control the sale process, whether through a traditional sale, short sale, or cash sale to an investor. Consider selling your house as-is, as this option can speed up the process by eliminating the need for repairs or appraisals. Cash buyers or real estate investors can close more quickly by buying the house in its current condition. Working with a real estate agent experienced in distressed sales can help you sell quickly and avoid further complications from foreclosure.

Sell to a Cash Buyer or Investor

Selling to a cash buyer or real estate investor is a fast and straightforward solution to foreclosure. Cash buyers often purchase homes as-is, with no need for repairs or extensive showings, which can significantly speed up the process. Unlike traditional buyers, cash investors can typically close within a few days or weeks, helping you avoid the risk of a foreclosure auction. While the sale price may be lower than market value, it provides a fast resolution and reduces damage to your credit.

Know Your State’s Foreclosure Laws

Understanding your state’s foreclosure laws is crucial when facing foreclosure, as each state has different rules and timelines for the process. In judicial states, foreclosure must go through court, taking several months, while in non-judicial states, the process is faster and handled outside of court. Some states offer protections, such as a right to cure or a redemption period, that can delay foreclosure. It is important to research your state’s specific laws and consult with a foreclosure attorney to understand your rights and make informed decisions.

Seek Professional Legal Help

When facing foreclosure, getting professional legal help is essential to protect your rights and navigate the process effectively. A foreclosure attorney can guide you through options such as loan modification or bankruptcy protection, ensuring the lender follows the proper procedures. They can also help negotiate directly with the lender or dispute wrongful foreclosure actions. Additionally, a HUD-certified housing counselor can help you understand relief programs and create a plan to address your financial situation.

How Do Foreclosure Laws and Selling Rules Vary by State?

Foreclosure laws and selling rules vary by state, including judicial vs. non-judicial foreclosures, mandatory notice periods, and protections like the right to cure and redemption periods. These differences affect the timeline and options available to homeowners facing foreclosure. For example, the right to cure may allow homeowners to reinstate their mortgage, while redemption periods provide extra time to reclaim a foreclosed property. Understanding these state-specific factors is crucial for homeowners to effectively navigate the foreclosure process.

Judicial vs. Non-Judicial Foreclosure States

Judicial foreclosures involve a court process that automatically makes the process longer, whereas non-judicial foreclosures are handled outside the court system, making them faster and more streamlined.

In judicial foreclosure states, like Florida, New York, and Illinois, the lender must file a lawsuit and obtain a court order, which can take several months due to court backlogs and legal requirements. In contrast, non-judicial foreclosure states, like California, Kansas, and Ohio, allow lenders to proceed with foreclosure through a trustee with the “power of sale” clause. This does not require court involvement and is typically completed within a few months.

Understanding these differences is crucial for homeowners facing foreclosure to determine the best strategy and explore available alternatives. Consulting a foreclosure attorney familiar with state-specific laws can help ensure you take the appropriate steps.

Mandatory Notices and Waiting Periods

Foreclosure cannot proceed without lenders following specific notice and waiting period requirements, which give homeowners time to take action and explore options to avoid foreclosure. Most states require a Notice of Default (NOD) after 90 days of missed payments, formally starting foreclosure. A Notice of Sale (NOS) is typically issued 20 to 30 days before the auction. Some states, like California, require a 30-day pre-notice, while New York mandates a 90-day notice. These notices must be delivered according to state laws, and failure to do so can delay or prevent foreclosure. Homeowners should review all notices and consult a foreclosure attorney to understand their rights and deadlines.

Right to Cure (Reinstatement)

The right to cure, or reinstatement, allows homeowners to stop foreclosure by paying the overdue amounts, including any fees and penalties, within a specific time frame. This gives homeowners a chance to catch up on missed payments and avoid foreclosure if they can resolve the default before the sale date. The timeline for reinstatement varies by state, but it typically occurs before the foreclosure auction. In California, homeowners can reinstate their loan up to 5 business days before the foreclosure sale, while in Arizona, the reinstatement deadline is 5:00 PM on the last business day before the Trustee’s Sale. Understanding your state’s reinstatement laws is crucial to acting within the required timeframe to prevent foreclosure.

Redemption Period by State

The redemption period is the time allowed for homeowners to reclaim their property after a foreclosure sale by paying the full sale price plus interest and fees. For example, New York and Florida do not offer a redemption period, meaning homeowners cannot reclaim their property once it has been sold at auction. In contrast, states like New Jersey offer a short redemption period of 10 days, while Minnesota provides a longer period of 180 days. States like California and Kansas offer redemption periods of up to 1 year, and in Tennessee, homeowners may have a lengthy redemption period of up to 2 years. Understanding the redemption laws in your state can provide an important opportunity to reclaim your home after the sale.

Deficiency Judgments

A deficiency judgment is a legal ruling where a lender seeks to recover the remaining balance on a mortgage if the foreclosure sale price is less than the amount owed. In states like California, Arizona, Oregon, and Minnesota, deficiency judgments are not allowed on primary residences after foreclosure, meaning the lender cannot pursue the homeowner for the remaining debt. However, in states like New Jersey, Florida, and Texas, lenders can seek a deficiency judgment if the home sells for less than the mortgage balance. Knowing your state’s laws on deficiency judgments is important to understand if the lender can pursue you for the remaining debt after foreclosure.

What Are the Financial Consequences of Foreclosure?

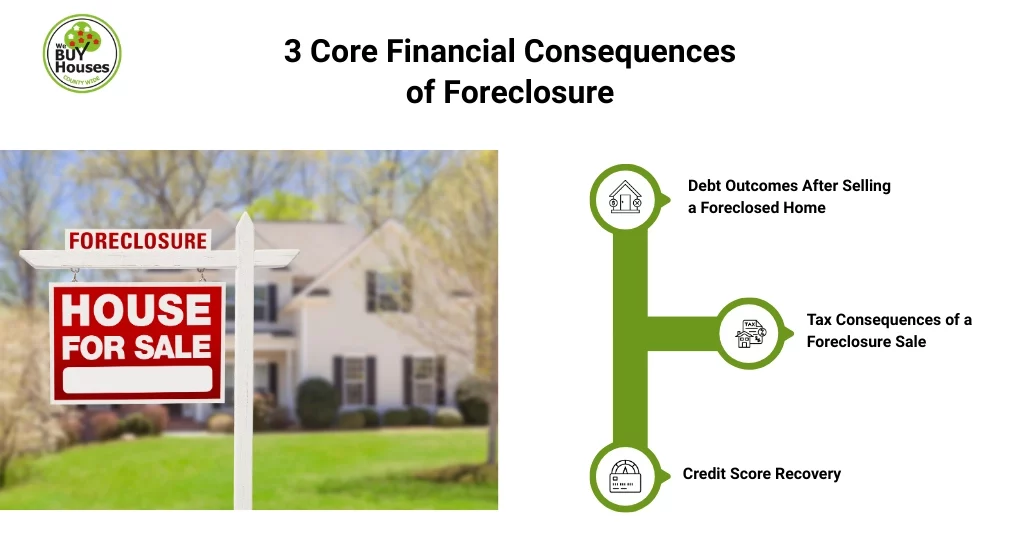

Foreclosure’s financial consequences include remaining debt, tax liabilities, and long-term damage to your credit score. After foreclosure, you may owe a deficiency balance if the sale does not cover the mortgage, and forgiven debt may be taxable. It also damages your credit, which can take years to recover.

3 core financial consequences of foreclosure are:

Debt Outcomes After Selling a Foreclosed Home

After a foreclosure sale, if the property sells for less than the mortgage balance, homeowners may still be responsible for the deficiency balance. In states that allow deficiency judgments, the lender can pursue the homeowner for the remaining debt, which can lead to wage garnishment or a lien on other property. However, in states like California and Arizona, deficiency judgments are prohibited for primary residences, preventing homeowners from being held liable for the difference.

Tax Consequences of a Foreclosure Sale

A foreclosure sale can have significant tax consequences, especially if the lender forgives part of the mortgage. The IRS treats forgiven debt as taxable income, meaning you may have to pay taxes on the forgiven amount, reported on a 1099-C form. However, programs like the Mortgage Forgiveness Debt Relief Act can exclude some forgiven debt from taxable income. The rules vary based on loan type and property, so consulting a tax professional is essential to understand the full impact of a foreclosure sale.

Credit Score Recovery

Foreclosure can cause a significant drop in your credit score, up to 160 points. It may stay on your credit report for up to 7 years, as per CFPB. The impact can make it difficult to qualify for loans or secure favorable interest rates in the future. However, credit recovery is possible with time and consistent financial management. By making on-time payments for other debts, reducing credit card balances, and using secured credit cards, homeowners can gradually rebuild their credit. Typically, credit recovery takes 3 to 6 years, depending on your financial actions and habits.

Why Immediate Action is Critical in Foreclosure?

Acting quickly in foreclosure is essential to preserve your home, minimize financial damage, and explore available alternatives. Delaying can limit your choices and increase the risk of foreclosure, leading to long-term damage to your finances and credit. Acting quickly allows you to address the situation before it escalates and gives you a better chance of finding a solution.

5 reasons why immediate action is critical in foreclosure:

- Preserving homeownership through options like loan modification or forbearance

- Avoiding foreclosure auctions by selling early

- Minimizing credit damage

- Accessing mortgage relief programs

- Seeking legal advice to understand your rights

FAQs

Can You Sell Your House to the Bank?

Yes, you can sell your house to the bank through a deed in lieu of foreclosure (DIL) agreement, where you voluntarily transfer the property to the lender to avoid foreclosure. This option allows you to walk away from the property without the foreclosure process damaging your credit as severely. Alternatively, if you owe more than the home’s value, you may be able to work with the lender to sell through a short sale, where the lender agrees to accept less than what is owed. In both cases, it is important to negotiate with your lender for approval.

Can You Sell a Foreclosed Home You Already Own?

Yes, you can sell a foreclosed home you already own, but the process depends on whether the foreclosure has been completed. Once the foreclosure is finalized and the property is transferred to the lender, it becomes a bank-owned property (REO), which can then be sold. If you still own the home and the foreclosure process has not been completed, you may be able to sell it through a short sale with the lender’s approval. The key factor is whether the foreclosure is finalized or still in progress, as this determines your ability to sell.

Can I Sell My House Before Foreclosure Starts?

Yes, you can sell your house before foreclosure starts, as long as the property is not already in foreclosure or auction. Selling early, especially if you are in pre-foreclosure, can help you avoid foreclosure and protect your credit. However, the sale must be approved by your lender if you’re behind on payments.

How Long After the Foreclosure Sale Do I Have to Move?

Once the foreclosure sale is completed, homeowners typically receive a 3-day written notice to move from the new owner or lender. This notice gives the homeowner a short period to vacate the property. The timeframe for moving out varies by state. For example, in California, homeowners may need to move out immediately after the auction, while in Minnesota, they may have up to 6 months to redeem the property. Understanding your state’s laws and the redemption period is crucial to knowing when you must vacate.

How Soon Can I Buy a House After Foreclosure?

You can buy a house after 3 – 7 years of foreclosure for conventional loans, or up to 2 years for VA loans, and 3 years for FHA and USDA loans. The waiting period can vary based on the type of loan and the severity of the foreclosure on your credit report. However, if you can show strong financial management since the foreclosure, you may be able to qualify sooner. Understanding the specific loan requirements and rebuilding your credit is key to securing a mortgage after foreclosure.

Can You Sell Your House If You’re Behind on Payments?

Yes, you can sell your house if you are behind on payments, but the sale must be approved by the lender. If the home is in pre-foreclosure, you can sell it through a short sale where the lender agrees to accept less than the owed amount. If the foreclosure process has already begun, you can still sell before the auction if the lender agrees to the terms.